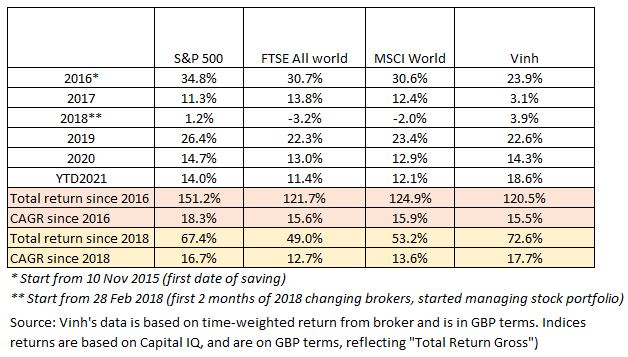

General

Q2 2021 has been relatively quiet. I continue to put capital to work into “old” ideas. These are the companies that have already been in the portfolio for quite some time.

Government bond yield, a key driver of valuation, continues to be low. Shortly after the end of Q2, the 10-year Treasury yield dived to 1.3%, from the high of 1.9%, owing to concerns of the ongoing spreads of the Covid-19 Delta variant.

The hurdle for equity returns is low. That said, I would stay vigilant of the fact that the 10-year bond yield reflects a very overpriced bond price (in nominal terms) ever seen in the history of borrowing and I would continue to use a discount rate of 6.0% to value all productive assets, instead of the 1.3% government bond yield.

“You don’t justify anything by taking the most overpriced asset in the history of man – the bond market, and say, compared to that, equity is not overpriced and relatively cheaper. That is very cold comfort” – Jeremy Grantham, July 2021

Business updates

Alphabet

“Our ultimate moonshot is still Search” – Sundar Pichai, Google I/O – May 21

Amazed at the research work in display during the Google I/O event, I found it interesting to learn that Search, the oldest business of Alphabet, is still in a “moonshot” phase.

Mr Pichai explained that at the moment, Search is still about looking at key words and giving users answers based on them. But, with Google’s conversation technology – LaMDA, short for Language Model for Dialogue Applications, the hope is to enable a free-flowing conversation between users and Search, and allow Search to really provide useful information to users in a more natural, human-like conversational way (https://www.youtube.com/watch?v=Mlk888FiI8A , 43:00)

Despite the exciting R&D efforts in display, we remain cognizant of the large size of Alphabet, and the resulting bureaucracy (https://www.nytimes.com/2021/06/21/technology/sundar-pichai-google.html ) developed from within.

Alphabet is expected to earn pre tax $104 per share this year. Compared this to the current share price of $2500, it is a 24x pre-tax earning multiple, which to me is still a reasonable price for a double-digit growing business.

In addition, if we adjust for the excess cash that it has on its balance sheet, and the loss-making but valuable Cloud and Other-bet segment, the multiple would go down to just 20x, which is the same level that many good low-single-digit-growth consumer goods companies are trading at.

My largest position continues to be Alphabet.

Facebook now has around 10m businesses that pay to advertise on its ecosystem, compared to 200m businesses that currently use its platform for free. In addition, it also has 250m users who are now engaged in ecommerce on its platform.

The other thing I note is that the core Facebook blue app registered noteworthy activities amongst its Groups/Communities, which Facebook executives have specifically called out on calls.

In addition, Facebook Reality Labs continue to make headlines, with the greatest revenue on record thanks to the Oculus Quest 2. The nascent VR efforts also account for most of the increase in R&D spending.

Overall, Facebook is expected to earn pre tax $16 per share this year, compared to the current share price of $350. This is a multiple of 22x. Adjusted for excess cash on balance sheet, rough estimate of value of Whatsapp and Oculus which are either not making any money or losses, the multiple drops further down to 19x. A very cheap multiple for a great double-digit grower.

Amazon

The major headline this quarter is of course that Mr Jeff Bezos will go on a space journey, leaving the key to Mr Andy Jessy who used to run the AWS business.

Reading into the background of Mr Jessy, he has been with Amazon since the early days, and have shadowed Mr Bezos for a long time before running the AWS business, which practically was built up from scratch.

His style of leadership is definitely different to Mr Bezos, but Mr Bezos’s track record would arguably be nowhere near where it is now had it not been down to Mr Jessy’s operating ability in scaling AWS.

Overall, Amazon this year is expected to earn pre tax $70 per share, but once allowed for the benefits of negative working capital business model, earn a cashflow pre tax $100 per share. Compared this to the current share price of $3700, this gives a multiple of 37x.

This is optically quite high compared to the multiples of Alphabet or Facebook. However, while the latter benefit from continued strong low to mid-teens growth in digital advertising, Amazon benefits from a high-teens to 20%-30% growth in all of its business: ecommerce, cloud and advertising.

Plus, Amazon, as it approaches the steady state, can decelerate its capex spending (mainly on warehouse and data centers) significantly, which would mean its free cash flow will start to take off.

I remain quite comfortable with Amazon valuation at the current level.

Blackstone and Brookfield Asset Management

The two private equity giants continue to benefit from the allocation to alternative asset management in the low rate environment.

Both have now jumped on the insurance business, providing reinsurance coverage whilst investing the floats that come in from collecting premiums.

We have learned from Mr Buffett and Mr Munger that “there are a lot of temptations to do dumb things in insurance” mainly because the lovely money come in in day 1 (you just need to grant people a promise and they will pay you premium), but that can be the last day you ever see that money if your premium is not adequate.

As we learn from Mr Ajit Jain, two things need to be understood well in writing insurance. 1/ the risk exposure and whether premium received is adequate and 2/ there must be a cap on your total liabilities. In the case of Brookfield, the recent insurance partnership that it did with AEL exposes Brookfield to maximum, $10bn worth of liabilities – Brookfield needs to insure $10bn worth of annuity policies. Brookfield receives this $10bn as cash in day 1 to start investing.

If Brookfield can earn an investment rate on this $10bn, that is higher than the costs attached to these policies (i.e. insurance claims paid out to policyholders), Brookfield makes money…and better yet, make money for itself with other people’s money.

One thing to note is that when Brookfield and Blackstone get to its current scale, both manage more than $500bn of AUM each, the reinsurance field only then becomes attractive. This confirms our previous knowledge from Mr Buffett that reinsurance, particularly insuring big big claims like $10bn worth of annuity policies or some major catastrophe, is only reserved to those who have the scale to do it. Berkshire, Brookfield and Blackstone are all very big to play well in this game.

Size matters!

The New York Times

The growth in the number of digital subscriptions at the NYT decelerated during Q1 21, as expected, following strong digital subscriptions gains during the election year and COVID.

There has been no major news, and I continue to remain watchful of its subscription activities, and its pricing potential.

The Times do $260m in free cash flow in 2020. If they can scale this to $1bn, which incidentally is equivalent to doubling the digital news only subscription base and achieving average subscription price (including introductory offers) of $12 a month (30% below the current full price of $17), it will be a great outcome for shareholders.

The maths on NYT potential work!

Book recommendation

My book recommendation this quarter is Dark Towers by David Enrich.

It captures the story of Deutsche bank and the people involved. The urge to replicate the personality of Wall Street in what was known as a boring German retail bank. The previous past involving funding the Nazi’s war efforts was discussed, as well as stories involving the ex US president – Donald Trump and Deutsche private wealth bankers.

It also highlights a great lesson of culture in banking, in which how the bank operates depends largely on the tone from the top.

The book also highlights great need for good corporate journalism, the work that Mr Enrich and his peers do in uncovering stories from relatives of the bankers involved are very interesting to learn about.