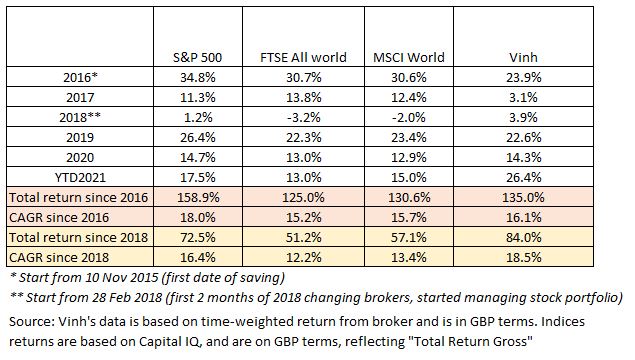

General

During the quarter, the yield curve continues to remain at around 1.48%, or an earning ratio of 67x.

The yield curve remains very low when compared to its history. This is shown below.

Source: https://www.multpl.com/10-year-treasury-rate

In fact, it is the second lowest point since 1870, or more than 150 years ago.

In real terms, the government bond actually yields a negative figure. Based on the current inflation figure of 5.3% which captures some “transitory” effects of the pandemic (note: I’m not exerting a statement that the current inflation of 5.3% is neither “transitory” nor “permanent”, as I do not know, it is just that there are “transitory” effects of the pandemic in that figure), the government bond in real terms yields a negative rate of close to -4%.

This is mind blowing. If you buy the safest asset in the world, it will deduct from your principal amount 4% a year, in real terms.

I’m not aware of any similar market condition in the history of finance. And like the majority of the population, I do not know all the effects it will unleash upon the world economy. Though, what I do know is that it certainly will have some distorting effects upon valuation and price of many assets, both productive and non-productive, around the world.

Having said that, I notice central banks have already started talks about tapering quantitative easing operations, and potentially nudging up interest rate. I do not know to what extent Mr Jerome Powell or whoever will succeed him, thinks the current inflation is “permanent” or “transitory”, but given such talks of increasing rate, there are certainly some degrees to which Mr Powell and his team think that the current inflation of 5.3% may contain some elements of permanency. To which, the rational course of response is to start thinking about increasing rate.

Given this market condition, I continue to be aware of central banks’ actions, though I do not spend more than 15 minutes each quarter (including the time writing up this blog post), pondering where rate may go. And I continue to use 6% as the appropriate discount rate to value any productive assets. This would give me a significant margin of safety should interest rate rise from its current level.

Interest rate is a very important yet unknowable factor in investing!

A mistake – Inditex

Towards the second half of 2019, I set out to buy shares in Inditex – the premier fast fashion brand headquartered in Spain but renowned around the world.

Since the second half of 2019 up until my disposal of Inditex shares in September 2021, I have realised a compounded annual return of c.11%, compared to 15% of the S&P 500, 13% of the MSCI World Index, and 12% of the FTSE All World Index (all figures include dividends and in GBP terms).

The stock has clearly underperformed all major indices. Let’s have a look at why (pandemic alert!)

In 2019, my rationale for purchasing Inditex was that:

- The company has strong competitive advantages around proximity-enabled inventory/distribution management, strong brand recognition and a global footprint;

- The company has good management who manages the firm conservatively (it started with a net cash position of EUR 6bn when I first bought the stock, and ended with EUR 8bn net cash when I sold the stock);

- Potentially very good growth opportunities by a/ expanding the selling space in a given store and b/ growing and integrating digital online operation with the existing brick and mortar stores.

In summary, I was hoping for a 15% compounded return that is made up of 3% space growth, 5% like for like sales growth, 2% expansion in operating profit margin, 3% dividend yield and 2% from earning-multiple expansion (e.g: I bought Inditex at 17x pre-tax earnings, 2% multiple expansion would mean this 17x become 19x over 5 years, hardly ambitious).

The first 2 were within Management’s long-term guidance, the op-profit margin expansion was based on my judgement that as and when Management scaled its digital online operation up it would benefit from some margin expansion, the dividend yield was what I was getting based on 2019 dividend payments and the multiple expansion would then be a direct result of the market perceiving Inditex as a 21st century tech-enabled fashion house once the digital online operation was to be scaled and integrated successfully.

Well needless to say, hardly any of this stuff happened, the reality of the return that I’ve got is -4% revenue decline (a combination of severe reduction in the like for like sales growth and minimal space expansion), -9% in operating profit margin contraction, +2% dividend yield (lower than my expectation by 1%), but +21% multiple expansion.

Obviously Covid has had a huge impact on the growth and management of the business, and I only have positive things to say about Management in terms of scaling digital operation to now 25% of total revenue while keeping op profit margin at a respectable 15%. Dividend yield was lower than expected as the business needed to conserve even more cash during the pandemic.

Though the multiple expansion, to the tune of 21% p.a., is interesting. This multiple expansion is a combination of a/ the market perceiving Inditex in a very good light as the company successfully integrated and grew its digital operation and b/ COVID threats have now subsided, with stores reopening, and in fact revenue started already trending even higher than the pre-COVID levels. It is important to note that at my disposal, the stock was trading at exactly the same earning multiple as when I first bought it, on a 2019-earning basis, i.e. on a pre-COVID earning basis.

Up until now, it doesn’t sound like owning Inditex was such a grave mistake.

Perhaps, the mistake lies in the opportunity cost. Clearly there have been more resilient, all-weathered and growing companies out there that I could have owned newly or more of. Yet, I chose to part roughly 5% of my portfolio with Inditex.

Perhaps in the next 3 years or so, Management will be able to carry out the things I noted above to get to a 15% CAGR return.

However, during the quarter, an opportunity appeared that I decided to sell Inditex to fund the purchase of this opportunity.

There wasn’t any cash in the portfolio to fund such purchase, hence I had to sell the least attractive company in the portfolio to fund the money.

I will talk about this opportunity more in the next quarter.

Book recommendation

The book for this quarter is the autobiography of Sir James Dyson – “Invention: A Life”.

Dyson is a household name in the UK, famous for vacuum cleaner products.

Of course, Sir James Dyson – the founder of the Dyson company didn’t want to spend the rest of his life building vacuum cleaners when he started out. Instead, he knew always that he was going to be an engineer. But engineer what?

I think this is the first thing that fascinated me. He knew he’s good at drawing, designing, taking things apart, etc, but he didn’t know exactly what he was going to build. I believe he just let it happen, he just let life show him what he was going to build.

That led him to a very unlikely candidate at first, which is to reengineer the ball barrow. He stumbled into the idea of reengineering the ball barrow while gardening in fact. What can be more about life than gardening, and what can be more mundane than rebuilding the ball barrow?!

And of course, with the heart of an engineer, as soon as he saw the many pitfalls of the then ball barrow, he set out to reengineer it.

This sort of establishes a pattern in his life. What things need to be reengineered in our daily life, pick the most mundane object, and he would go and fix it. There’s no need to do any market research!

The other thing I found interesting about Sir James Dyson was that early in his career, despite catching the first big break very early when the Rotork company founder – Jeremy Fry took an interest in him and helped advance him quite quickly, Sir James Dyson appeared to be a little reckless in his finance.

He and his family did go into major debts, using their own house as leverage to fund a prototype of the ball barrow mentioned earlier, to which he did lose out a costly legal battle with the company via which he tried to retail his product, and just barely got enough from the litigation process to pay back the debts.

I certainly would not do that…but then I would never become a world-class inventor as Sir Dyson.

But what he compensates for the financial recklessness was the determination of an inventor.

The famous story is that Sir Dyson tested 5,127 hand-made prototypes of his cyclonic vacuum, which finally led to the creation of the DC01 – Dyson first vacuum cleaner product that practically blew everything else off the shelf (though not until many months and years of hard work convincing retailers to stock his products on the shelf).

Upon the DC01, he and his team improved on it. The engineering culture was so strong that at one point, the DC12 (the 12th version of the DC01) is powered by a motor “with a power-to-weight ratio five times greater than a contemporary Ferrari Formula 1 racing car”.

Think about it?! What sort of young men would follow a guy who set out to build a motor for vacuum cleaner that is more powerful than that used in a luxury racing car? Certainly, there are a lot of them who would eventually follow Sir Dyson.

Overall, the book is great to read, and I’m sure student of engineering would love to read how Sir James Dyson describes the nuts and bolts of inventing things. There are a lot of such stories, and I must admit I do not understand all of the technical. I’m sure I have missed out on a lot of engineering brilliance from the book. Yet I still very enjoyed it.

Hope you would enjoy the story too!