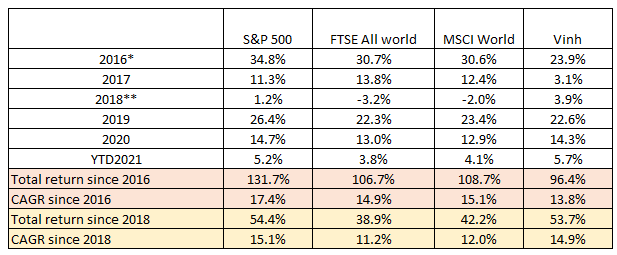

** Start from 28 Feb 2018 (first 2 months of 2018 changing brokers, started managing stock portfolio)

Source: Capital IQ (Indices are based on GBP, Total Return Gross price)

General market

“The biggest risk of all is the possibility of rising interest rates. The downward trend in rates is over (if we can believe the Fed’s assurance that it won’t take nominal rates into negative territory). Thus, while interest rates can rise from here, they can’t decline. This creates a negatively asymmetrical proposition. Can the 10-year Treasury note still yield [1.75%] if inflation reaches 3.0%?” – Howard Marks – 2020 review memo (adjusted slightly to update for the latest 10-year yield)

The most significant market development in Q1 2021 was the rise in interest rate, as measured by my favourite yardstick – the 10-year Treasury bill yield. The yield has gone up significantly, from 0.9% as at 31 December 2020, to 1.75% as of writing. One can inversely deduce that the valuation multiple of the 10-year US government bond has declined significantly, from a price to earnings (“PE”) ratio of 111x to 57x. If this was seen as the bar over which an equity investor needs to clear before buying any stocks, the bar would now rise higher.

What does this all mean? It means that whatever corners of the equity market that have seen their valuation stretched to 111x or higher (during Q4 2020, one of these corners was noted to be the cloud/ software-as-a-service stocks), they will now see significant valuation pressure. And, indeed we have now seen a significant pull back:

New York Times (“NYT”, or “the Times”)

During Q1 2021, I started buying stocks of the New York Times.

I became familiar with the NYT around early 2018, when I first finished reading Mr Buffett’s shareholder letters. I remembered he said that one of the 5 newspapers he read daily was the NYT. I’ve got a clue and immediately started following the Times since then.

A year later, what was happening at the NYT, operationally and financially, started to hit me!

I immediately sent a short investment email pitch about the NYT to David (Arche Capital), whom I mentioned in past blog posts. The email is as follow:

“Date: Fri, 22 Mar 2019 at 23:06

Subject: The Times as a branded product

Hi David,

Hope you are well.

I’m having this thought after having followed the NYT for the past year and taking a huge interest in their journalism.

In the past quarter call, it occurs to me that NYT is morphing into a “consumer branded product” and the “untapped pricing power” lies in their unique position of high-quality journalism, longevity and a huge “displacement” tailwind, the latter is measured by [the] number of paid subscribers (4.3m) vs the global audience, ie the number of users who actually uses the NYT monthly but do not pay (130m!).

From 2012-2018, Mark Thompson [the Times ex CEO] has increased SG&A (mainly headcount growth in journalists and marketing) by just 3% p.a, [yet] he scaled from 0 paid subscribers to 4.3m (currently growing at a good clip at 20% p.a).

Mark [Thompson], an ex-BBC chief, has not broken his promise. He said he would double digital revenue (both digital subscription + digital ad) from $400m to 800m$ in 2020 and in 2018 he already reached $700m.

He recently promised that he would scale the number of paid subscribers to 10m from the current 4.3m by 2025, so 6 years from now.

What are the chances that one of the best investigative award-winning journalism newspaper can ask [an additional] 4% of their global audience to pay for it? (an additional 5.7m paid subscribers as % of 130m global audience)

That will be $600m revenue flowing directly to gross profit. Then if I assume SGA is to grow at 3% p.a in the next 6 years, then pre-tax earnings in 2025 will be around $630m, or [effectively, the share price represents just] 8.7x 2025 pre-tax earnings.

What do you think?

Thanks,

Vinh”

I sent David this email when the NYT was selling for roughly $4.5bn in market capitalisation, about $25 a share. The stock is now $50 a share, a nice 41% CAGR in 2 years.

But, don’t congratulate me yet!

The plot twist is…I did not buy a single share!

I did not buy a single share, despite having the understanding of their unit economics, that any $ incremental subscription revenue earned from a new subscriber will more or less flow directly to the bottom line. Afterall, you do not need to hire 1 new highly paid, highly qualified, award-winning journalist to cater 1 new subscriber.

Whilst this unit economics is being talked about a lot when a cloud type company is in question, it is mainly wishful thinking for the most part. To attain this amazing unit economics, one has to have 1/ a ton of money to spend on marketing initially, then 2/ have an awesome product that is sticky, and 3/have a huge “white space” to just run away. Now, these criteria can be immediately recognised and can be assessed right away by someone who works in the field as one can use their first-hand knowledge to assess these 3 criteria. However, I for one don’t work in the cloud industry and for another, I realise that, even if I quit my finance job to jump into the cloud industry, I probably won’t be able to understand it anyway.

Though luckily, there is one company that is not in the cloud field, but directly benefits from this unit economics, and that I understand.

And that is the 170-year-old NYT.

The NYT is no longer an advertising-dependent company. It now is a consumer-branded product company with a subscription unit economics attached to it. This is best of both worlds: the world of beloved consumer brands with pricing power and the world of cloud companies with awesome unit economics.

The NYT brand

“On the walk back, Graham [of the Washington Post] explained that [Warren] Buffett did not think there was room on the web for a second digital American global newspaper and thought the Times would always be number one there. The “Supreme Court” has handed down is ruling” – Jill Abramson – Merchants of Truth: Inside the News Revolution

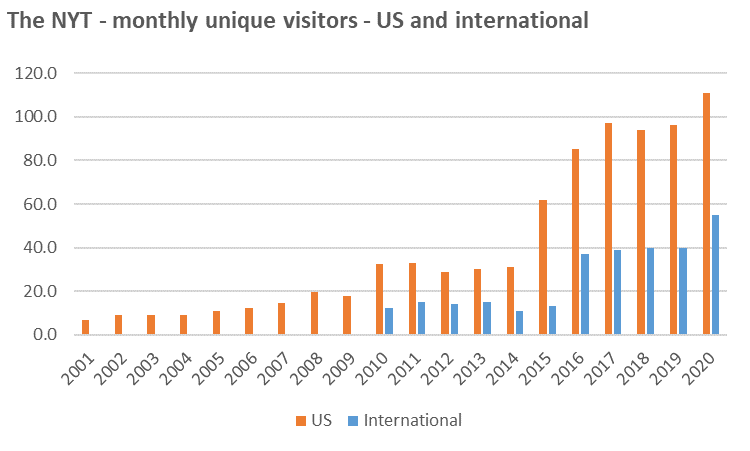

The chart below shows you just how wonderful the brand has gotten at the NYT, in their home market – the US and also internationally.

During the US election week in Nov 2020, 273m global readers came to the NYT, higher than even Fox News and CNN (link)

A good consumer brand not only is present in millions of minds of consumers around the world, but it should also have the ability for great pricing power over time.

Decades ago, during the golden age of newspapers, such pricing power was measured through how much the paper could charge its advertisers. Today, it is measured by the price charged on each subscription.

Imagine a x-y axis chart, where on the x-axis, you have “the monthly price per one NYT subscription”, and on the y-axis, you have “the degree of familiarity, from very-new-to-the-Times to can’t-live-without-the-Times”. The resulting curve on this chart will be very steep:

- For a completely new subscriber to the NYT, the subscription costs as little as £2/month;

- For a non-US, yet familiar subscriber to the NYT, who has read the NYT for quite some time, but only reads the digital version, he or she will pay around £8/month.

- For a US digital only subscriber, he or she will pay roughly £12/month (or the official price tag of $17/month).

- For some very familiar subscribers who have spent their entire adulthood reading the Times and want 7 day a week paper delivery of the NYT all year round (think Charlie Munger and Warren Buffett), the price could be as high as $80/month.

That is one hell of a steep pricing curve. Depending on which part of the audience the NYT is dealing with at one point in time, management can effectively experiment around which point on this curve they want to charge!

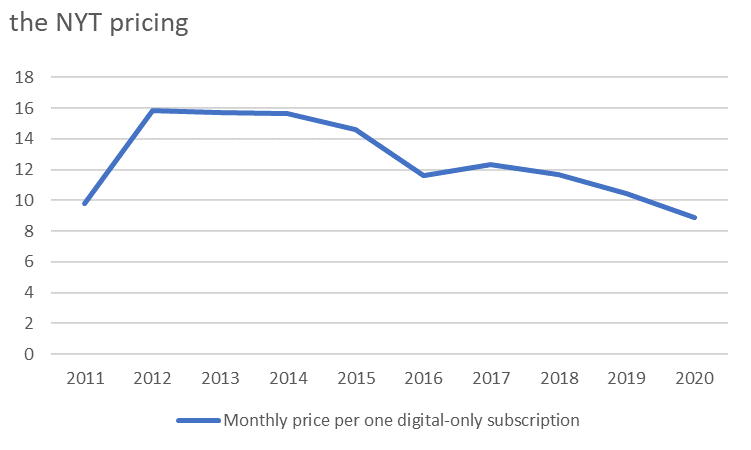

“What do all of these translate into the current price per one digital sub, at the company level?” you may ask.

Not so good, at least historically speaking:

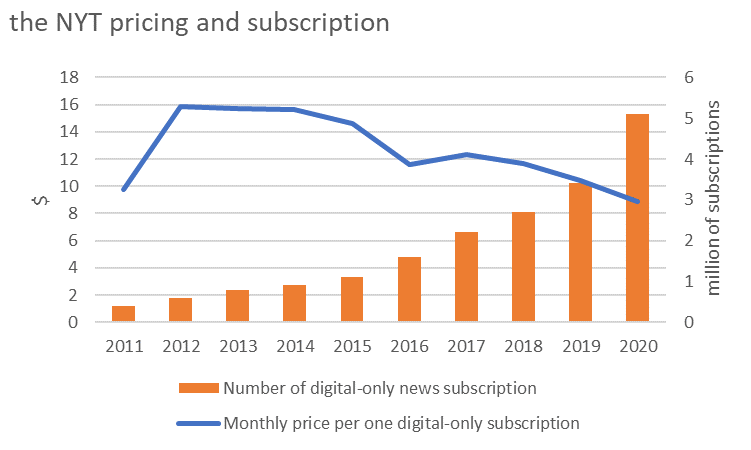

But this alone is misleading. The full chart needs to also show the growth of the number of subscriptions as well:

That is very encouraging! The number of digital-only news subscription has grown from 400 thousand subs in 2011 to 5.1 million subs by 2020, a 13x increase in a decade, even though average price per subs remained broadly unchanged, at $9-10 a month.

Note, despite the declining digital price per sub trend from 2012 to 2020, there has been no discount given to the ones that already pay the full digital price in the US of $17/month. The price is trending down rather because the NYT is onboarding a lot of new readers, such as those in the category number 1 above, by giving these new readers heavily discounted price. So, the price is skewed downwards, and in effect serves as “marketing costs” to gain new subscribers who could stay with the Times for a long time, as long as the quality of journalism is maintained.

Critics to this strategy talk about the risks that new subscribers may cancel very quickly after their discounted subscription expires.

My answer to this is, yes…if the quality of the journalism is not maintained.

Interestingly, the strategy that the NYT is pursuing now is very similar to the same strategy that it pursued way back in the 1900s when the NYT was still much smaller than other national newspapers:

“The World and the Journal each cost two cents an issue. [Adolph Ochs – the former published and owner of the NYT in the 1900s] could not match either in [Spanish] war coverage, so he would compete with them in price. Ochs announced that he was dropping the price of the Times, so serious and respectable and priced accordingly, from three cents a copy to one cent.

It was a stroke of genius. Some said that the paper was seeking a new audience and would start to sensationalize the news. Some of the Times reporters, restless with the prohibitions against being stylish, were overjoyed. But they were wrong, and Ochs was right, the paper remained what it had been, and the circulation soared. Ochs defended his decision by pointing out that once the paper was put together and ready to print, it cost him less per copy to print 100,000 copies than, say, 40,000, that the real expense came before the first issue was printed, the cost was in the printers and stereotypers. It was a stunning victory. The Spanish-American War, ironically enough, was the making of the Times. A year later Ochs’s circulation was 76,000, triple what it had been before he cut the price.” – David Halberstam – The Powers That Be.

History doesn’t exactly repeat itself, but it does rhyme!

The lesson is that you gotta try your best to onboard as many new readers as you can, and have trust in the journalism you have built, and they will then stick with you for a long time. That first article they read on the Times expose them to world-class journalism for the very first time, and that will stick as long as the quality of the journalism is maintained.

Having said that, there is significant potential for the Times to actually, raise price!

In fact, to measure the potential for a price increase, one can look at the price charged to the heavy readers of the NYT. This can be roughly measured by the price per sub of the “print based bundle” segment (i.e those that read both print and digital) of the NYT. The price per one print-based bundle subscription has grown from $37/month to $55/month between 2011 and 2020, i.e. a CAGR of c.5.0%!

All in all, I feel very comfortable that an institution like the NYT, which has existed and delivered quality, “hedgehog”-type news for nearly 2 centuries, will continue to do what it does, and better yet in a transformative way that is completely adapted to the digital 21st century.

To quote Mr Mark Thompson – ex CEO of the NYT, a “hedgehog” knows one big thing in depth, instead of a “fox” who knows a lot of things but understands nothing – the fox is like Buzzfeed, or other news aggregators in general.

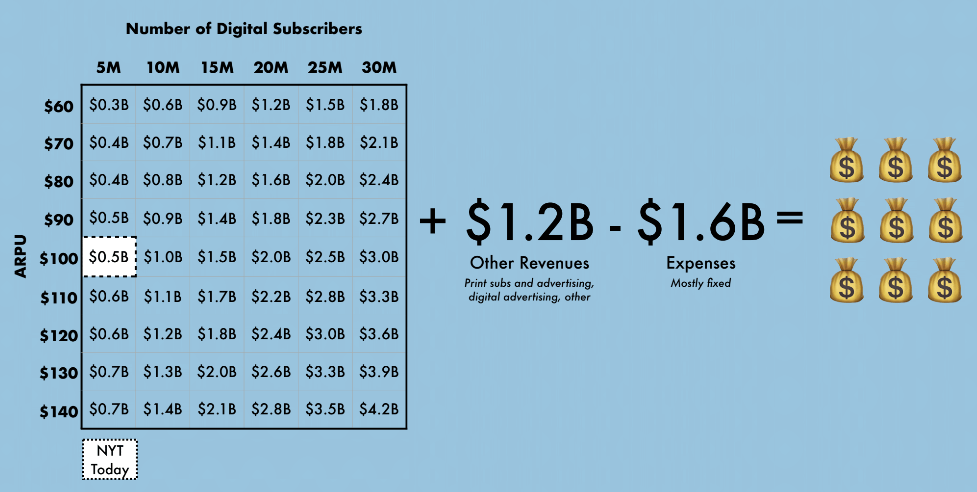

NYT Valuation

I built a detailed NYT financial model, so just drop me a comment and I will share it with you. But I would say don’t even bother with my model! Someone on the Internet has made a short and concise way to value the NYT. This is shown below:

You can then apply your own earnings multiple to those $$$ bags, to get to a target equity value.

Disclaimer: Given that this sounds like an investment recommendation, it is NOT! I just want to clearly state here that I’m not recommending buying nor selling NYT shares. This is merely a personal post in a blog that documents my investment journey. So please do your own research.

Book recommendation

A book recommendation for this quarter is “Leadership” by Doris Kearns Goodwin. As a newbie to American political history, I have thoroughly enjoyed this great book, which chronicles the major events in the lives of 4 great American presidents: Abraham Lincoln, Theodore Roosevelt, Franklin Roosevelt and Lyndon Johnson.

The book is wonderful because it discussed in great depth the psychology and behaviours of these men as natural leaders when facing personal and political storms, starting from their early childhood to when they become presidents. In this book, I particularly enjoyed the chapters that talk about:

- Abraham Lincoln’s childhood as he grew up poor and was denied to knowledge by his own father. He would walk miles and miles to get to a library to read books. Unlike today when a great book is only a click and a few quid away;

- Theodore Roosevelt’s ability to cope with despair as he lost his mother and wife in one day. I can’t hardly imagine the agony that one would have to endure through such event;

- Franklin Roosevelt’s natural optimism and internal realism as he dealt with his illness – polio. He was always cheerful according to the eyes of the witness, and eventually set up a hospital where he was called “Doc Roosevelt”; and of course, the times when;

- Abraham Lincoln, as president, freeing the slaves with the Emancipation Proclamation while winning over hearts and minds of many of his critics by skilful use of language (his story-telling skill was well-known), together with great temperament and compassion: he issued a lot of pardons to forgive the ones who fought against him during the civil war, constantly trying to find one good reason to spare a man’s live; and

- Franklin Roosevelt’s extraordinary leadership throughout the Depression in the 30s. His extraordinary and skilful use of the radio to communicate with the public during the Depression must be noted! unlike how some president mis-use social media throughout the COVID-19 pandemic!

Great comprehension & analysis em! I am amazed at the Times’ paid subscribers for its crosswords & cooking as well. Agreed it shifts to consumer branded company with a right time based on cloud era. It is still the quality journalism, but how it has chosen to change the medium to serve: paid content digital with less dependent advertising. More importantly, it has known very well who are its read paid customers: subscribers, not advertisers, and is doing the best to serve what they pay. It also changes the dynamics of accounting for the newspaper business – to solve the real business issue: fixed cost with cloud infrastructure, not the variable costs (printing, content development etc.) which a lot newspapers are in trouble.

LikeLike