The comeback

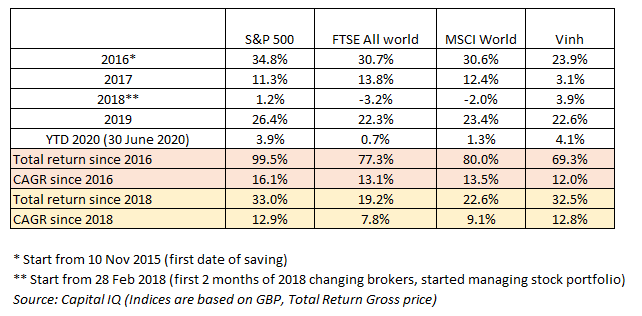

As noted in the Q1-2020 blog post, we would have bought more stocks even on a monthly basis if our base case had happened. Instead the worst case happened. The worst case is characterized by the c.40% increase in the S&P 500 from its trough of 2237 at the end of March 2020.

“Maybe the second-most overvalued stock market I’ve ever seen” – David Tepper – Appaloosa Management – 13 May 2020 CNBC interview

The market price level is now roughly at where they were at the beginning of 2020, though their earnings are not. Simple arithmetic would show that the valuation multiple of the S&P 500 has deteriorated.

When we started 2020 we were out of action, having seen stocks climb a whopping c.30% in 2019. Now as stocks broadly are at the same level as it was 6 months ago with earnings being down some 30% by analysts’ estimates quasi-retirement from near-term capital deployment seems to be as real as ever.

The unknowns

It’s quite important to stress the number of important unknowns .

Source: Uncertainty memo – Howard Marks – Oaktree Capital Management – 11 May 2020

A simple I-don’t-know attitude would probably save investors a lot of troubles. We try not to make mistakes of the investors who immediately make investment decisions by wearing their epidemiologist/virologist/central banker/politician hat on. We are simply not well placed to make investment-related decisions by utilizing our little-to-nil knowledge in pandemic, virus, monetary policy and politics. We will try to stay well inside our circle of competence, and that is to make investment decisions based on what the businesses are and do.

Around end of March, early April, a lot of the important unknowns were compensated quite fairly by Mr Market, as a great many high-quality companies were sold for high single digit to low teens multiple of their pre-tax, pre-Covid earnings. One can simply deduce that these companies, in the environment of 1% interest rate, can be worth as much as 20x+ their pre-tax, pre-Covid earnings figure.

Effectively that leads to the question: “when will they regain their pre-pandemic earnings power?”

Simply expecting that these companies will able to regain their 2019 earnings by 2024/2025 isn’t unreasonable given that most forecasters expect some sort of normalcy between 2021-2023.

As such, the price level around March and April does have significant margin of safety built in, and indeed it was a great opportunity to be more aggressive in buying stocks. Therefore, over the short to near-term, I would expect that our gain would largely be driven by an expansion in earning multiple accompanied by a recovery in earning power.

It is true that the good time to buy stocks is generally when you have the money, as there were only a few time when stocks were obviously overvalued compared to risk-free assets. Though for the “enterprising” investors, the good time to aggressively buy stocks was that of March and April time.

“There have been four great buying opportunities in my adult lifetime. The first was in 1973 and ’74, the second was in 1982, the third was in 1987 and the fourth was in 2008 and 2009. And this is the fifth one” – Bill Miller – Miller Value Partners – 18 March 2020 CNBC interview

And buy we did!

Net, I deployed roughly 12% of my portfolio. The biggest chunk of the cash went into Facebook – a company I admire and have been their user for the last 10 years. The remaining of the cash has gone into largely existing positions and perhaps 1%-2% have gone into new positions: Carmax, Brookfield Infrastructure, and AG Barr. They were clearly cheap at the prices they were at.

But the opportunity was very brief.

The portfolio

During this quarter I was invited to host an investing webinar for the Vietnamese professional community. The investing webinar was held along with other skill-based webinars to raise money for an NGO.

In the investing webinar, one of the messages I would like to convey to the audience was to convince them to focus on the real business progress rather than the stock price when investing.

To uphold that spirit, I will focus on the real business progress of a few selected companies in my portfolio over the past 6 months.

Though judging real business progress through the lenses of 180 Earth days can be misleading, but in any case, it does help emphasize the importance of watching the business, not the stock price. Further if the corporate world only lets me watch its progress on a quarterly basis sure I will be glad to take full advantage of doing just that.

Facebook is our pandemic biggest stock purchase, we were super excited for being able to have a great entry price into being a part owner of this formidable business, ran by an intense management team which is headed by a product-driven young CEO.

We think our edge in owning Facebook compared to the average opinion of the market is such that we have an appreciation of Facebook’s hackathon culture which, by design is destined to churn out more and better features for both users and advertisers over time.

“It’s the engagement, stupid!”

During the quarter, we also saw new features released by Facebook to drive more user and advertiser engagements such as Facebook Shops and Facebook Gaming, along with many other smaller features that aren’t newsworthy but are proof of continuous improvements of the platforms.

We think that rather than asking the question “What’s next?” or “What else can Facebook create?” one should just kick their feet up and enjoy the many features that Facebook will release over time. Some will flop but more often than not a few big wins will carry the engagement curve upwards.

One of the lowly monetized assets at Facebook is Whatsapp – the messaging service that Mr. Mark Zuckerberg bought in 2014 for a hefty price tag of $20bn. Since its acquisition, the users count at Whatsapp has grown from 500m to 2 billion users, a compounded annual growth rate of 25%. In relation to Whatsapp, during the quarter Facebook announced a major minority stake acquisition in Reliance Jio via Jio Platform Limited – a company with 388m 4G subscribers, effectively 65% of India’s 4G mobile market. The deal capitalized Jio at around $170 per users and at around 28x EV/ annualised 19-20 EBIT (Q4 19-20 EBIT grew c.50% y-o-y) . While optically it looks high, we would refrain from concluding the deal is expensive on a statistical earning multiple basis, yet even then 28x statistically doesn’t look neither expensive in a world of below 1% interest rate nor cheap. Overtime we will see what Mr Mark Zuckerberg could do in leveraging this relationship with the existing 400m Indian users that are already on Whatsapp.

Google Cloud Platform and G-Suite: I’m excited to see that Google has executed not only strong growth at the Infrastructure as a service level but also at the platform as a service level with its Data and Analytics offerings. In addition, management also noted strong growth in both volume (seat count) and pricing (revenue per seat count) for G-suite – a collaboration/software as a service offering which I’m a daily user through my full-time work. Overall, management continues “shooting the light out” with its cloud offerings, and the cloud business’s revenue is up 52% year on year.

Berkshire Hathaway

Due to work restriction, it is quite likely that I will have to sell Berkshire in December 2020. Until then we will continue to report on the firm’s progress.

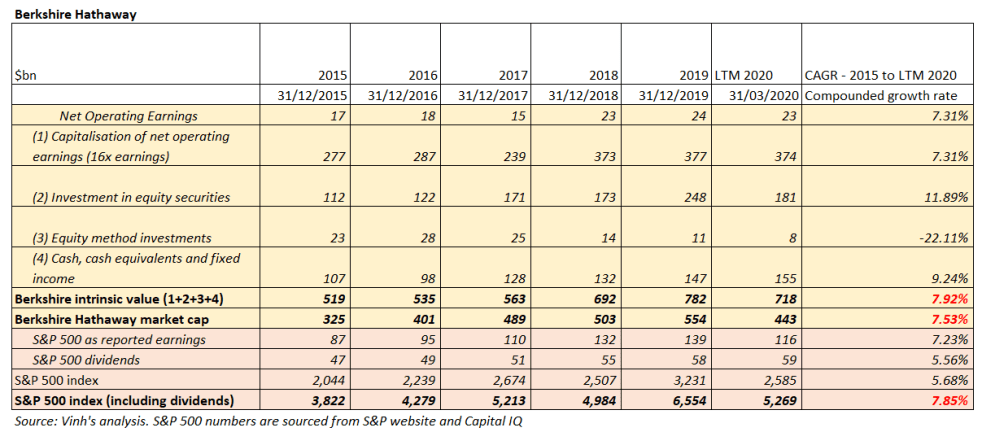

Over the past 5 years, we note that Berkshire’s capitalisation has tracked well with its real business progress.

One of the highlights of the Q1 2020 is our first online attendance of the Berkshire Hathaway 2020 annual meeting. We, together with other observers and watchers of Berkshire, noted that it was probably the first time ever that Mr. Buffett’s tone was that pessimistic. Though he remained the usual long-term American optimist, in the short to medium term and as careful as a word chooser as he is, Mr Buffett said:

“you better, not be too sure of yourself about what it’ll do in the next six months or year or whatever”

Having gone through all the Berkshire meeting records since 1994, I did not remember coming across such a bearish tone from him. Yet rather than interpreting this as saying this is the time to sell stocks we agree with Mr Andrew Roskin of the New York Times’s assessment of Mr Buffett’s tone:

“Warren Buffett’s Optimistic? Pessimistic? No, Realistic”

Brookfield asset management

“It is ludicrous to think that companies will not return to offices. Anyone who says they’re not going to be in offices is naive about how company culture is built. Brookfield – office serves as a place to build culture” – Bruce Flatt – Brookfield Asset Management – June 2020 Reuters interview

“The problem is that the tenants [of the malls] have not innovated as quickly as the market has changed and the result is that all [sic] of corporate stores that have been around for 100 years that haven’t innovated to attract customers and I do think malls from any community are are public gathering spaces and you just have to have tenants that are interesting enough to inspire people to come together and either shop or be entertained and I do think that innovation is happening, it’s just not happened as quickly as [the speed] that the legacy tenants are dieing” – Bill Ackman – Pershing Square – Bill Ackman: Getting back up [The knowledge project Ep.#82] – Farnam Street

The real estate business, especially that in retail (Brookfield) and office building (Brookfield and Blackstone) are taking damage from the lockdown orders worldwide. Whilst retail was already a troubled type of asset as retail space is undergoing multi year transformation as the quality of the retailers improve, I also agree with Mr Bruce Flatt that office space is required to build business culture. I also haven’t seen that many companies publicly announcing permanent work from home as an option other than the like of a few such as Twitter and still do think office building is important in a post Covid world.

As a colleague of mine is fond of saying “I buy that!”.

Blackstone

“In real estate, logistics now represent over one-third of our entire portfolio positioning us well the benefit from the powerful global growth in e-commerce.” – Jon Gray – Blackstone Group – Q1 2020 earning call

Logistical real estate has a big tailwind ahead of it with the growth of ecommerce and being as shrewd as he is, Mr Stephen Schwarzman bet big on it with other people’s money.

At the same time, Mr Schwarzman intensely focuses on growing “permanent capital”, something that we also see Mr Bruce Flatt does. This and the inherent attractiveness of the switching cost of the PE business should gradually increase the earning multiples on the AUM of Blackstone that is subjected to performance fees:

“Different than the normal money manager you give money to and they invest it for you and when you wanted back, they mostly give it back to you. And some people, lock it up for short periods of time, 30, 60, 90 days, sometimes a year. But basically, you can get your money back if you’re in liquid securities. We, for the most part, not all of our business, but for the most part are involved with private securities. So you can’t get your money back immediately. And so what we’ve done as an industry is raise money where we can keep that money for very long periods of time; in many cases, 10 years or 12 years. And about 20% of our money is in perpetuity. And so we have a completely different model for running our business, which is that our management fee income is remarkably stable compared to loan-only manager, if you will, or a credit manager, because you can always take your money back if you don’t like them. And so that cash flow stream gets a really great valuation because it’s around for so long.” – Stephen Schwarzman – Blackstone Group – Bernstein’s 36th Annual Strategic Decisions Conference

Union Pacific Railroad

“I’d say, when we look at our overall cost structure, I can say almost with some certainty. The one area the cost structure that’s virtually fixed, at least in any kind of near-term, medium-term is depreciation. After that, we have the ability to move every — most everything else. We’ve got a fixed asset base that generates that depreciation; but when you think about adjusting our cost structure for 25% down in volume, that’s matching our train, engine and yard [expense] to that and then some, which we’ve done.” – Lance Fritz – Bernstein 36th Annual Strategic Decisions Conference

I was pleasantly surprised by the flexibility of the railroad cost structure as the management team there continue driving operating ratio down and down. Management noted that operating ratio stood at roughly 59%, an improvement compared to last quarter and last year as they continue working their way down to 55%, and just when I thought 55% is the max that you can go…

“Yes, I wouldn’t talk to 55 is the limit, for us it’s a target…We haven’t put a date on it. We also know the end game winning long-term value creation is about increasing cash flow generation, which comes from increasing operating income. So, that’s where our crystal clear focus is and we think we need to get that both with top-line with productivity, and with price.” – Lance Fritz – Bernstein 36th Annual Strategic Decisions Conference

Book recommendation

A book recommendation this quarter is an old book: Idea man, a memoir by the co-founder of Microsoft by Paul Allen

I have thoroughly enjoyed Mr. Paul Allen’s memoir. His journey started from being in the forefront of a new industry as the world shifted from mainframe to personal computer, the cut-throat competition in the Wild Wild West of personal computer, his difficult yet rewarding partnership with Mr Bill Gates, all while dealing with the struggle of a health scare to his passion for sport and his journey as an enterprising tech investor.

It’s also quite interesting to see how Paul Allen had many doubles in his investments, like being early with AOL or the online ticketing business. Yet one single costly mistake is enough to clean out all your gains. And surprise surprise, the biggest mistake that extremely smart and talented people like Paul Allen tends to commit has a lot to do with leverage!

“It’s not right for you to get half”, [Bill] said. “You (Paul) had your salary at MITS while I did almost everything on BASIC without one back in Boston. I should get more. I think it should be sixty-forty”

“They put me (Bill) in a holding cell and you (Paul) are my phone call” he said. “Can you get me out? It’s terrible in here!” Picked up for speeding on Central Avenue, [Bill]’d given the arresting officer a hard time and was thrown in with the drunks.

“If a hardware company used a BASIC that wasn’t ours, we’d disassemble it to see if they’d reverse-engineered our copyrighted code. If our suspicions were confirmed, a stern letter or two usually sufficed. If the code came from another company, we’d press the point that our BASIC was light years better. And it was, because we’d never stopped striving to add features and improve it”

“Steve Ballmer forcefully framed the company’s strategy in the mid nineties: “[The competition] can be taken. But the only way we’re going to take them is to study them, know what they know, do what they do, watch them, watch them, watch them. Look for every angle, stay on their shoulders, clone them, take every one of their good ideas and make it one of our good ideas.”

“My net loss in the cable business was $8 billion. Most of all, I failed to understand the downside of over-leveraging”.