Portfolio

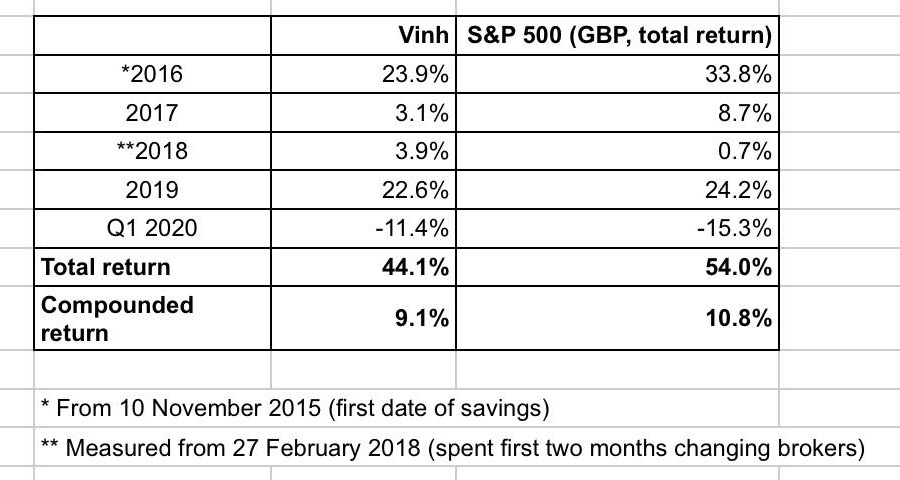

As mentioned in previous quarters, I continue to trek along and to slowly close the underperforming gap. The record started at the same time I started my first full time job and had real money to save. I started with a combination of passive and active funds, then moved to owning individual stocks in 2018.

Somehow I got the idea of tracking my financial performance as soon as I started investing. In the long term, I hope the record would not only track performance but also the learning progress.

As Steve Pinker noted: there’s a good argument for reason, science, humanism and progress.

The coma

The first quarter of 2020 saw the world economy go into a coma. Businesses shut down almost worldwide in response to the Covid-19 outbreak.

In my short investing career, I have had the chance to experience 3 meaningful declines in the stock market:

- the Chinese debt panic in 2016

- the trade war in 2018

- the Covid-19 outbreak in 2020

The latter created the steepest fall in quoted prices of marketable securities. Interestingly, accompanying these 3 falls are steep rises in between:

- the Vietnamese stock market, a market which I have always had a keen interest in, increased by 50% in 2017 with the IPO boom

- the worldwide FOMO period in the stock market post 2018 in 2019

These rapid rise and fall in the market is a testament to the existence of the “manic, depressive, drunken Mr Market”. Mr Market is still alive and well ever since Ben Gram introduced him in the 40-50s in his wonderful book “The intelligent investor”.

Even though I have lost count of the number of times Ben Gram’s A star student – Mr Buffett made reference to Mr Market, it seems like the world still underappreciated Mr Market’s very human behaviour. When he’s excited, he will not care about real corporate progress. And when he gets scared, he completely loses his head.

And with that being said, I tried my best to take advantage of Mr Market’s teenage-like mood, rather than letting him instruct me of what to do.

Actions

With the dislocation in q1 2020, I had the chance to deploy the 20% cash noted in my 2019 round up. In the coming months, as lucky as the position I am in where a gradual stable job provides monthly savings, I figure I can quickly save and work up to a 10% cash position in 5 months time. If the market continues to move sideway (such will be my base-case scenario, best-case scenario would be a further decline in the market) then monthly cash deployment will be much easier. Compared this to 2019 when there wasn’t any meaningful buying since everything was sold at pretty steep price.

Most of the cash have gone to existing positions and new positions. The shopping cart, in value order is approximately as follow:

- BX

- BAM

- Banks

- Bookings

- Unilever

- Union Pacific Railroad

- Visa

- Southwest

- Brookfield Infrastructure

- Inditex

- AG Barr

These purchases happen in a valuation range of 6x -16x pre-tax, pre-Covid earnings with an exception of 20x for Visa.

Overall such range is ”reasonable” and I would consider the financial rewards stemming from future underlying operating performance of these companies will be less likely to be undone by any mistake of overpaying.

At the above range, and with a 6% discount rate (in today’s world where rate is at 1% or below), if I’m right about the “economic moats” of these businesses, then all of their future growth will, in retrospect, be deemed as free. This simple perpetuity formula is once discussed in an executive annual letter as follow:

Therefore, reported earnings (before amortization of intangibles) were also freely-distributable earnings, which meant that ownership of a media property could be construed as akin to owning a perpetual annuity set to grow at 6% a year. Say, next, that a discount rate of 10% was used to determine the present value of that earnings stream. One could then calculate that it was appropriate to pay a whopping $ 25 million for a property with current after-tax earnings of $ 1 million. (This after-tax multiplier of 25 translates to a multiplier on pre-tax earnings of about 16.)

Now change the assumption and posit that the $ 1 million represents “normal earning power” and that earnings will bob around this figure cyclically. A “bob-around” pattern is indeed the lot of most businesses, whose income stream grows only if their owners are willing to commit more capital (usually in the form of retained earnings). Under our revised assumption, $ 1 million of earnings, discounted by the same 10%, translates to a $ 10 million valuation. Thus a seemingly modest shift in assumptions reduces the property’s valuation to 10 times after-tax earnings (or about 6 1/ 2 times pre-tax earnings).

1991 Berkshire Hathaway annual letter

Some reading and listening over the past quarter

“When Genius Fails” – Roger Lowenstein

It’s a wonderful story of the rise and fall of Long Term Capital Management. I attached my notes here.

When Genius Fail – Vinh Nguyen notes

“Facebook: The inside story” – Steven Levy

Following Mr Levy’s book on Google – “In the plex” I was super excited to read his story on Facebook. My notes are attached here.

Facebook: The inside story – Vinh Nguyen notes

It’s the engineering culture that creates these behemoths. Constantly adding useful features that drive user engagement is the key to garner eyeballs. A sound engineering culture (and it almost has gotta come from the top, in this case Mr Zuckerberg) enables this.

2019 Berkshire Hathaway Annual Letter

Never fail to be the most anticipated CEO annual letter.

https://www.berkshirehathaway.com/letters/2019ltr.pdf

Bill Gates on Ted Talk speaking about Covid-19.

I posted my notes on Bill Gates talk on FB:

“Just what the doctor ordered!

Few lessons:

- Contagious but not as deadly

- Testing, testing, testing (on the symptomatic)

- Right equipment for nurses and doctors

- Isolation

- “Herd immunity is meaningless until you affect half of the people”

- “Extreme shutdown” (unless you got number 2 right)

- “to keep it below 1% of population, it’s really only two things: testing and isolation”

- Economy: “bringing money back is more of a reversible thing than bringing people back to life”

- Therapeutic – “Out of the top 20 or so candidates, probably 3 or 4 of them will work out at different stages of the disease to reduce the respiratory distress”

- Antibodies of the recovered: “compared to drug that we can make on high volume, logistically it’s hard to scale the numbers”

- “the wild card is how the developing countries deal with this”

AlphaGo movie

I was actually in tears watching this movie. It’s sensational.