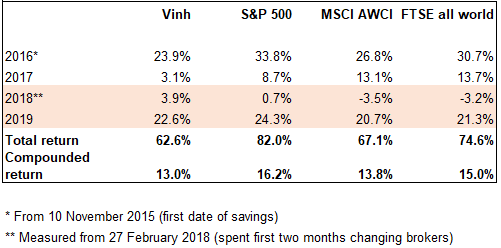

The portfolio increased 22.6% for the year, compared to 24.3%, 20.7%, and 21.3% of the S&P 500, MSCI ACWI and FTSE All World total return (GBP) indices respectively. (“The indices”).

Since inception, the portfolio has compounded at a 13.0% rate vs 16.2%, 13.8% and 15% of the indices.

From 28 Feb 2018 (when I started picking individual stocks), the portfolio increased 27.3% vs 25.2%, 16.5% and 17.4% of the indices.

There is still a fair amount of catching up to do as I’m trying to bridge this underperformance gap since I first had any real money to save and invest.

My expectation still remains. I’m willing to underperform now and to learn as much as I can so that in the far future if I ever get to manage other people’s money, I will then be well equipped to create value. Any underperformance now is tuition fees paid to the university of marketable securities where the headmaster is the mood-swinging “Mr Market”.

Another thing to note is since Feb 2018 the number of mistakes have been limited to mistakes of omissions. Whilst I still expect to commit mistakes of commission in the future it does go to prove that in the investment game, avoiding big costly mistakes of commission is the key.

Another point to note is that this decrease in the number of mistakes coincides with when I started learning from the right investing teachers. This includes reading Berkshire Hathaway annual letters and attending its annual shareholder meeting, meeting David – my mentor in mid 2017, then subsequently meeting with his mentor – James in mid 2018, following great investors who have established long term track records, and just generally more reading. The job for me now is to make sure this continues for as long as possible.

“Name of the game is continuous learning” as Mr Munger puts it.

Challenge for 2020

The current portfolio currently has 17% in cash. This build up of cash is as a result of earnings and savings coming in rather than because of any selling during the year. I have been struggling to find good opportunities to deploy in 2019. There were a lot of obvious gold nuggets in late 2018 as Mr Market turned depressive and sold out a lot of great companies. Apple for instance, one of the biggest companies in the world, was fetching at less than 10x pre tax earnings whilst it was intending to acquire 16% or so of its own stocks. Opportunities like this were hard to come by in 2019 as the S&P 500 and other relevant world market indices took off from its low to finishing the year at 20%+ total return.

My backlog of top ideas are currently banks (buying more 8x pre tax earnings BAC and WFC), hands-on asset managers (12-16x earnings BAM), reasonably priced well-run insurance companies (10x pre tax earnings Progressive Corp), unique content owner (16x pre tax post-registration fcf Manchester United, 8x unlevered earnings Discovery, 6x pre tax earnings ViacomCBS)

Other holdings in my portfolio are also an obvious source of ideas, however most are trading at valuation I neither want to top up nor sell. Except for Apple, which is currently trading at close to 20x pre tax earnings which I’m hoping to redeploy a significant part of it to some of the above mentioned opportunities.

“If you look at the success of Berkshire, it is really just one to two ideas every 2 year” – Mr Munger.

FAANG

Our portfolio owns all the media- labelled FAANG companies except for Netflix. Such holding of seemingly popular names do not speak for my underlying enthusiasm of being a part owner in these businesses. These businesses almost require no major capital to grow and they are inherently good businesses. Their return on tangible capital are all eye popping numbers.

Facebook earns $23bn in operating profit on a tangible capital of $30bn, ie a 77% return on tangible capital. It is a great “engineering” company with a “hackathon” culture that is hard to be found elsewhere. Hundreds of features are added to an already-strong ecosystem of Facebook, Messenger, Instagram and WhatsApp only to strengthen the strong network effect in place. The business has pricing power in the pricing of advertising space to advertisers and has products that billions of people elect to watch every day with their eyeballs. Time waits for no one but some 1.6bn people do choose to spend a significant amount of their time on the Facebook ecosystem everyday. Facebook excluding cash, is trading at 17x next year pre-tax earnings, or at less than 15x next year pre-tax earnings with a conservative estimate of WhatsApp. It is priced reasonably. It still has a strong tailwind coming from high-single digit growth of the world digital advertising market.

Apple earns $64bn in operating profit on a tangible capital of $40bn, ie a return on tangible capital of 160%. It is a design led company whose brands are very hard to match in the consumer electronic field. This design culture has been translated into success after success with the IPod, IPhone, IPad, Airpod and other accessories. I’m a little sceptical of the recent content push by Apple as “their content is thin,” to quote Mr John Malone of Liberty Media. But Apple is a rare company who can tinker and fail and as Mr John Malone also points out “people will be surprised at how quickly they will scale their number of subscribers”. Apple is currently trading at 19x pre tax earnings. At this price I would like to see Apple repurchasing share more sensibly. The underlying business should be able to grow at mid single digit top line as the IPhone sales slowdown stabilises whilst other products continue to grow at double digit. Apple can then buy back about 5% of its stock at this current price every year. Another 1% dividend yield and hopefully some margin expansion can add another 1-2% growth in earning power. This would lead to a total return of 13%+ in earning power. At this price therefore I think Apple is sensibly priced.

Amazon earns $20bn in free cash flow while employing $24.4bn in tangible capital, ie 82% return on tangible capital. And yet the business on a top line basis is still growing at 20%+. Amazon is a customer obsessed company of Mr Jeff Bezos who, as Mr Munger put it is “a miracle worker” as he single handedly dominates 2 industries: e-commerce and cloud computing. There are a lot of hidden earning power in Amazon as Mr Bezos takes all the earnings he could get his hands on to 1/ drive more volume in Amazon marketplace through lightspeed shipping, 2/ please audiences visually with content on Amazon Prime, 3/ building out more capabilities at AWS at the PaaS and SaaS level and more computing power at the IaaS level. As Mr Bill Miller puts it “3-5 years from now Amazon market cap may just reflect the value of AWS”.

Google (Alphabet) earns close to $40bn in operating profit while employing a tangible capital of $69bn, ie a return on tangible capital of 58%, and still growing on a top line basis in the high teens. It is also a great “engineering” company with lots of earning power hidden underneath. Its Android ecosystem is a $400bn mistake of Mr Bill Gates, its current $3bn annual run rate losses on “other bets” can be worth a great deal, with Waymo for instance leading the driverless arm race while its closest rival – GM Cruise sports a valuation of $20bn at the latest funding round. Alphabet, selling at 17-18x next year pre tax earnings is also sensibly priced.

Netflix though not owned in my portfolio captures my curiosity as Mr John Malone puts it as one of the two companies that will be around and be dominant in the medium term, together with Disney of Mr Bob Iger. $14bn of content acquisition budget is a lot, it’s basically almost all of Netflix revenue. Such amount is an awesome sum spent to please customers visually with great series after great series. However, at a valuation of 8x revenue, I continue sitting on the sideline and cheering for Mr Reed Hastings as he goes on “throwing Hail Mary passes.”

Book recommendation: “The ride of a lifetime” by Bob Iger – CEO of Walt Disney

It’s a book packed with insights. Mr Buffett used to describe Disney that “it’s an interesting business when once in a while you recycle Snow White and it hits a different generation”.

This “Snow White recycling” strategy has been carried out with lots of successes and mistakes by Mr Iger as he navigated the content world from his days at ABC/Capital Cities, learning to program unique content in sport, tv show programming to when he headed Disney, learning to “Snow White recycle” the characters at Marvel, Lucasfilm and of course the characters at the Pixar animation studio.

“I love the guy” – Steve Jobs told his wife about Mr. Bob Iger as he went over his decision to sell Pixar to Disney