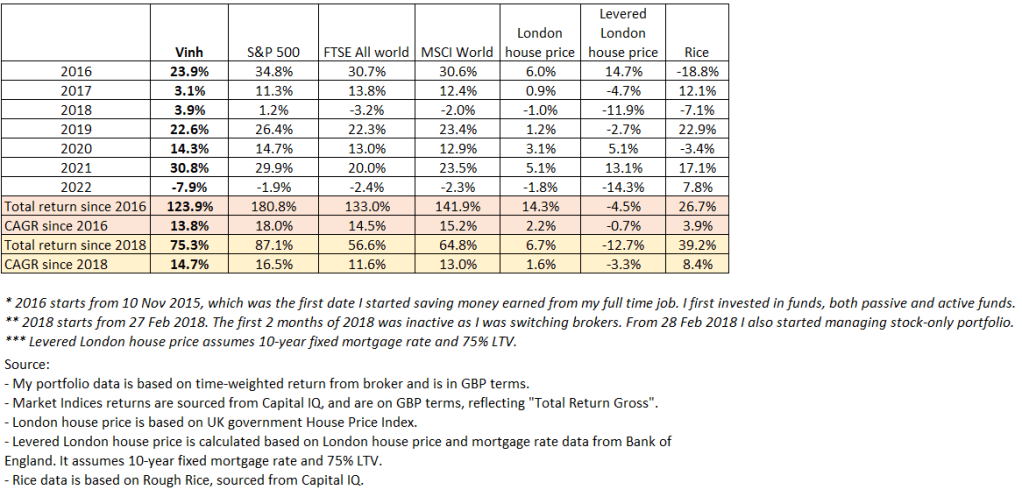

General

First quarter of 2022 saw major geopolitical event, with the Russian military invading the country of Ukraine.

Like many have said, it is a tragedy. I continue to watch the developments there with my heart going out to the Ukrainian people.

As Russia invaded Ukraine and sanctions have been imposed on the Russian government, companies and wealthy individuals, this led to major disruption in the O&G market which sent oil price to the height of $130 a barrel.

Looking back to 2020 when oil price briefly went negative, versus an oil price of $90+ a barrel now, it does reinforce my thinking that I can never predict where oil price is going to go.

That said, this doesn’t prevent me from buying O&G stocks in the future. Needless to say, when oil price was negative, it was also a very attractive environment to be thinking about an investment in that sector.

However, there were also other things that looked incredibly attractive then, and so opportunity cost remains a good filter for investment opportunity.

With commodity price hitting new highs, coupled with inflation on the rise, I saw key interest rate benchmark increased significantly also.

The 10 year US treasury yield increased from 1.6% to 2.3%. In effect the 10-year US government bond is now trading at a multiple of 43x (inverse of 2.3%), compared to 63x (inverse of 1.6%) a quarter ago.

One interesting data point, the 30-year fixed rate mortgage in the US went from 3% to now close to 5%! Optically that looks very high, and I don’t think the effect has yet trickled through to the data, as the latest data still showed a double digit increase in house price in the US. (despite the fascination with economic developments in the US, I have now become a UK citizen as of last quarter!)

I continue to use a discount rate of 6% to value all productive assets. I do not like the idea of using different discount rate for different assets, as it would defeat the purpose of using opportunity cost as a filter.

Business development

Meta Platform (formerly known as Facebook)

I would be remiss not to mention Facebook this quarter.

From a share price perspective, the stock has declined by about 30% year to date, with most of that decline coming from a one-day drop after the company announced its 2021 full year results and first quarter 2022 guidance.

The guidance gave a range of 3% to 11% growth in the top line, and a full year 2022 operating expenses guidance between $90bn – $95bn.

Under the low end of this guidance, FY22 revenue would come in at about $120bn, and operating profit of $25bn. This would represent a decline of 46% (1) in earnings compared to FY21 operating profit of $46bn.

Doing the same math on the high end gives you an operating profit of $40bn, or a decline of 13% (2).

Taking a simple mid point between (1) and (2) gives you a decline of 30%, same as the decline in the share price.

Taking with a pinch of salt on this mathematical coincidence, the market is effectively saying that the decline in share price reflects the decline in next year earning power, and that such decline reflects a permanent loss in the normalised earning power of the business.

But I do not think such decline is permanent, and hence I continue to own Facebook stock.

I do think that the earning power of Facebook will take an U turn after FY22, for the following reasons:

- The impact of the IDFA changes will foster a new era for first party data. And Facebook does have one of the biggest trove of first party data. Facebook still does $120bn in ad revenue (c.30% of global digital ad spending) despite the third party data business gets completely destroyed by Apple IOS14 change.

- Facebook continues to work at “closing the loop”, or as David Wehner – Meta CFO called it “on-site conversions”.

- The impacts of TikTok on Facebook and Instagram are real. But Facebook doesn’t sleep at the wheel and does have a strong product in Reel to counter it. From a business owner perspective, I do not mind it being a “copy” to TikTok, with incremental improvements to follow. At the end of the day, “great artists steal”, to coin Steve Jobs.

Facebook currently is trading at 12x FY21 EBIT, or 10x FY21 EBIT if I exclude the $10bn losses in Metaverse investment. It is very cheap.

However, I have not added to the position.

For one thing, after the fall in the share price, it is still a big position in my portfolio and for another, I do want to monitor the progress of Facebook on the three points above before adding further to it.

This is motivated by a balance between me seeing the management team at Facebook as very paranoid – a desirable trait, versus me seeing them as completely mismanaging the business.

So far, I attach a much higher probability to the former than the latter.

Other businesses

Our other businesses, being Alphabet, Amazon, the New York Times, Brookfield Asset Management and Blackstone are all doing very well.

Couple of highlights:

- Despite being the oldest business, Search at Alphabet is still a “moon shot” investment. I like it very much that the management team at Alphabet continues to invest to make Search better and better, and more human like with their latest AI advancements.

- Amazon broke out its Advertising business revenue for the first time, though we all know the big scale of Amazon’s advertising business already. This business currently does $30bn in revenue, and if Alphabet and Facebook’s operating profit margin serve as an indication, then Amazon advertising business will have an operating profit of $15bn plus. What would you value a business earning $15bn that can grow at 20%+ CAGR a year for the next 3-5 years?

- The New York Times acquired the Athletic for $500m, in effect acquired a unique 1.5 million subscribers who currently pay around $5 a month to read sport news and analysis. The New York Times do not have a great track record of M&A, yet the logic of this purchase is sound: bundling the Athletic with the New York Times subscription can enhance the stickiness of the subscription. I would continue to monitor for management’s efforts on this going forward.

- Brookfield Asset Management and Blackstone had a great year, with record inflows in private assets. The secular tailwind of governments hiring managers like Brookfield and Blackstone to manage their private investments will be a decade-long trend which would continue to benefit Brookfield and Blackstone. And despite the run up in their share prices over the past couple years, their valuations, at around 16x-20x annualised earnings (including performance fee stream) are not demanding.

Book recommendation

This quarter book recommendation is called the Genius Maker by Cade Metz – a NYT technology journalist.

The book traces the story of couple of individuals who pioneered in the research of AI. It is a great human story, digging deep into their passion to make data talk, to them navigating a world that increasingly comes to appreciate their unique talent as more and more data get stored and accumulated.