Great investing lessons were generously shared by some of my most favourite investors during January and February. For a complete list of the investors whom I admire, click here.

Lindsell Train “Insights” column – Comfounding Compounding

I’m a big fan of Lindsell Train – a UK-based investment fund run by 3 exceptional investors. The 3 managers follow a quality-investing philosophy and have had an exceptional track record investing in UK, World and Japanese equities. Once in a while they would publish new articles which address a varying range of investing issues from economic moats to valuation. One of the recent articles on valuation, written by James Bullock serves as a great reminder to how long-term investors should approach valuation (link). With Unilever as an example James deconstructed total return (capital appreciation and dividend return) into 2 key elements: multiple expansion and dividend/earning growth. Arguing that as little as 10% of the total return was explained by multiple expansion and the rest came from dividend/earning growth, James highlighted an important lesson: more often than not investors look solely at multiples as a judgement of valuation. Value investors, in particular would get more excited in finding a company with multiples less than 20%-50% of that of the market than a great company (more often labelled as boring or bond-proxies) with above-average multiples. They then neglect or pay little attention to the sustainability of earnings, and thus rely entirely on 1-3 year multiple correction as their main source of capital growth. Yet if we deconstruct historical total return of great companies (those with strong competitive advantages) we would then realise that almost 80%-90% of total return come from earning/dividend growth rather than valuation expansion. It’s actually pretty easy to see why as multiple expansion is limited (you can raise your PE until only a certain point, say 30x, historically speaking) but earning/dividend growth is not; e.g: Pepsi’s earning per share grew from $0.67 in 1990 to $4.63 in 2016.

Pat Dorsey’s portfolio – Superior capital allocator

Ever since Pat Dorsey started his own investment fund it has always been my interest in uncovering his holdings. Pat Dorsey was Morningstar’s Equity Research Director and wrote 2 books on economic moats, making him my most favourite business teacher. I find his generosity admirable. His teaching of moats, concisely summarising key factors that need to be looked at when assessing competitive advantages is the main source of inspiration to my current investing philosophy.

Since leaving Morningstar he has indicated that he would move from focusing 100% on economic moat to a mixture of 3 things:

- Economic moat

- Valuation

- Superior capital allocation (management knows how to smartly reinvest excess cash)

Out of the 3 what interests me most is superior capital allocation. Capital allocation refers to how well company’s management utilises excess free cash flow. This could be used to reinvest in existing business operation, acquiring new companies or paying dividend. This is an edge on which a narrower-moat firm could leverage much better than a wide-moat one. Think of it this way: with a narrower-moat company, superior capital allocation will help transition it to a wider-moat one, during the process the company would realise superior return that is even better than one generated by a wide-moat firm. This way of thinking is also noted to be the driver of small-cap investing, looking for high-growth companies that have enough potential to become a mid- to big-cap, during the transition investors would realise superior capital appreciation that, in the short- to medium-term underwhelm returns of larger firms.

His portfolio as of now:

Howden Joinery Group – UK-based kitchen and joinery products manufacturer, averaging less than 30% in dividend payout in the past 5 years

Roper Technologies Inc – an industrial conglomerate with more than 40 different businesses

Brookfield Asset Management Inc – Notable infrastructure investment firm with less than 35% dividend paid out in the past 5 years

Cimpress N.V. – customizing specialist with 100% reinvestment rate

Ansys Inc. – engineering-related software provider averaging 0% dividend payout

The Descartes Systems Group Inc – federated network and logistics technology solutions service firm, 0% dividend payout and significant M&A activity on an annual basis

AVEVA Group plc – UK-based engineering-related software provider

Facebook Inc – Need no introduction, no dividend, 100% reinvestment rate

With an exception of AVEVA Group the remaining companies have several similarities: high reinvestment rate and M&A focus. Both requires superior capital allocation skill in order to sustain above-average shareholder return.

Berkshire Hathaway’s 2016 annual letter – a £1m bet

The owners of Berkshire need no introduction so I will just go straight to the learnings.

There wasn’t anything completely new in the latest letter, instead the letter is used as a reminder. Here are some interesting quotes from the Sage:

“Every decade or so, dark clouds will fill the economic skies, and they will briefly rain gold. When downpours of that sort occur, it’s imperative that we rush outdoors carrying washtubs, not teaspoons. And that we will do”

>>> Remind me that I don’t need to invest in anything if I don’t absolutely have 100% confidence. Wait around and sooner or later an attratively priced “moat” company will be available. When this happens I will have to make sure enough time is spent on detailed research and valuation scrutiny, and of course press the “buy” button firmly and confidently.

“First, widespread fear is your friend as an invetor, because it serves up bargain purchases. Second, personal fear is your enemy. It will also be unwarranted. Investors who avoid high and unneccessary costs and simply sit for an extended period with a collection of large, conservatively-financed American businesses will almost certainly do well”

>>>Simple lesson: have a watchlist of amazing enterprises then buy them at almost certainly “bargain” price in bear markets. Valuation readjustment and subsequent earning growth would guarantee above-average compounding return. Additionally investors should avoid unneccessary costs via active trading or excessive fees charged by active-trading funds. These costs add up over time, causing uneccessary compounding losses. Save those pennies and reinvest in wide-economic-moat businesses instead.

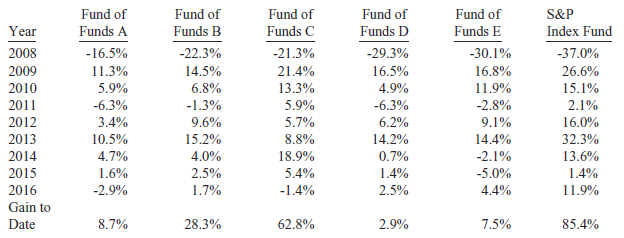

One couldn’t just write about Berkshire 2016 letter without mentioning Warren’s famous bet against Ted Seides – owner of the Protégé Partners LLC. You can find information on the bet here.

Background: Warren bet against Ted that S&P 500 would outperform a collection of hedge funds over a 10-year period. This collection of hedge funds was agreed between Warren and Ted and the 10-year period was from Jan 2008 – Dec 2017.

Result

S&P 500 beat the hedge funds by a wide margin. It’s interesting to also note that Ted argued for the risk-minimising benefit of hedge funds. Whilst certainly the standard deviation of all the hedge funds seemed to support the argument, risk-adjusted returns (measured by Sharpe ratio) were significantly lower than S&P500. Return in fact must be taken into the risk equation. Look at return as opportunity loss on pursuing less-volatile investments. Thus Sharpe ratio is relevant in quantifying the risks of any investment and from this perspective hedge fund investments made no sense.

…and that’s the end of today lessons. Class dismissed!