Today we will be looking at Wells Fargo, a company whose shares I recently bought amidst the negative headlines that you might have come across in the news these days.

I will outline the 4 key reasons why I bought the company

Before dwelling into WF, a brief background of what has happened with the company: Wells Fargo was found to have had 5300 employees who had created phony deposit/credit accounts and charged customers for products/services they had not requested. The bank was liable to pay a fine of $185m and refunded $2.6m to affected customers, on average $25 per one affected account. WF’s CEO resigned as a result and the stock dropped roughly 20% when the news were uncovered.

Before spending 2.5 weeks researching WF, I actually was looking at another company within the tech space for my final purchase for 2016. Yet with the price of the bank dropped drastically, I was caught up in thinking this may present an attractive entry point to hold shares of the best bank in the US. After all, the company has been around for 164 years with 10% of its shares being held by Warren Buffett.

So here are the 4 key highlights of my 2.5 weeks research and why I made a decision to buy the shares

Brand

WF definitely has a brand in the banking industry. It has $1.2 trillion in deposits of customers like you and me and of business customers. This leads me to think that the company may possess a valuable moat that cannot be easily replicated by others. Yet, Chase and Bank of America, Citigroup also have roughly the amount of deposits that we see at WF. So how can we make good comparison between these banks’ brands? And many other regional banks as well.

Well, to solve this, I followed the brand analysis that I outlined in my other post (“Just a thought”). A company with a moaty brand should be able to raise price consistently without sacrificing its own volume. In the banking space, banks just can’t raise price visibly due to interest rate is nearly being dictated by the market. However, what I can look at is to look at whether the price the banks charge the customers (ie interest paid on loan) is higher than the rest of the market and whether volume as a result stays flat, increased or decreased.

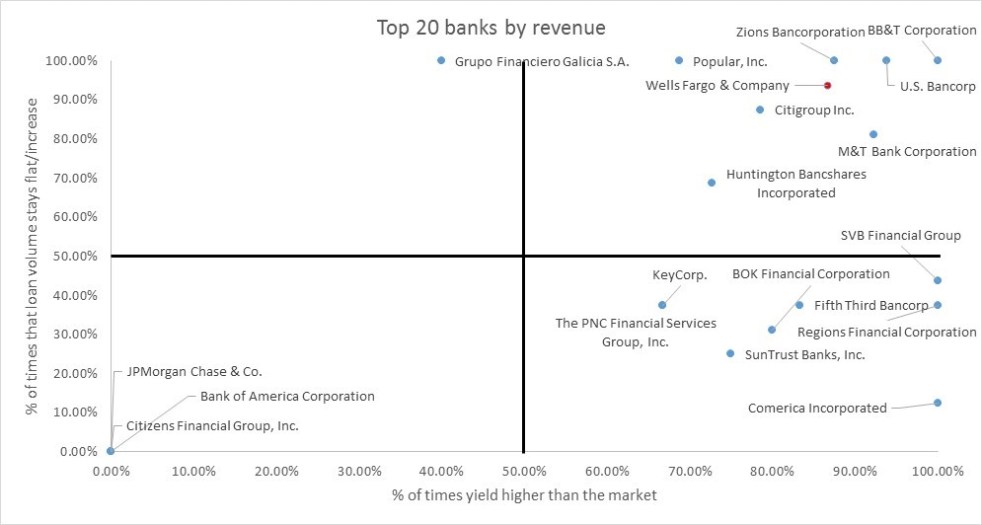

Take a look at the graph below. The X axis shows the number of times yield (interest on loan) is higher than the market and the Y axis shows the number of times that volume stays flat/increased within the times that yield is higher than the market. This is based on data going back to 2000, so a total period of 16 years.

Wells Fargo has 93.75% of the times that its yield were higher than the market. This means out of the last 16 years, the yield that Wells Fargo charged its loan customers were higher than the rest of the market for 15 years (16 x 93.75%). It then has 86.67% of the times that loan volume stayed flat/increased in the 15 years that its yield was higher than the market ie 13 years of volume growth with increase in price (15 x 86.67%). These 2 numbers are remarkable as they imply that the brand is so strong that customers are willing to pay higher interests just to be loaned by WF.

Notice how only Citigroup is the only other big bank that has great branding while JP Morgan and Bank of America’ brands are the worst. The 2 couldn’t have price higher than the market and therefore volume growth has been purely driven by low interest rate offered on its loans.

Also notice that the top right section of the graph shows some other banks whose brands are as great as Wells Fargo. These include US Bancorp and Citi as diversified banks and the rest are all regional banks.

Within the diversified banking space, I would therefore pick US Bancorp as you can see it has higher brand advantage compared to Wells Fargo. However, taking other reasons into account, you will soon see why US Bancorp is not as moaty as Wells Fargo.

Cost advantage

The next factor we are going to look at is the cost advantage that banks enjoy.

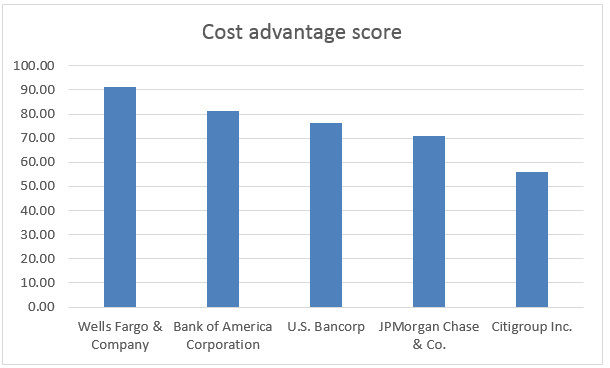

Have a look at the table “Cost advantage score” below. In this table, I attempted to quantify the strength of WF’s cost advantage relative to other diversified banks.

The cost advantage scores are made up of 6 categories with equal weighting – ie the max score per category is 16.67. The 6 categories are:

- % of low cost funding: banks that have significant funding sources coming from low-cost deposits (money from checking/saving accounts) will stand at a significant competitive advantage to others

- Interest rate on deposit: with low cost funding, I would expect to see the bank also has low interest rate paid on its deposits

- Interest paid on funding sources: same as interest rate on deposit but this one looks at interest rate on the total funding source (so including external borrowings)

- Absolute amount of low-cost deposit: the first category is relative, this one is absolute number

- Revenue per employee: with high amount of deposits come high revenue generated on banks’ resources. The key resource here would be the banks’ employees

- Cost per employee: same as revenue per employee but in opposite direction

Wells Fargo came up top in the first 3 categories and third in the other three. In total, it has the highest cost-advantage score across all the big diversified banks.

If we now compare these 5 diversified banks to the rest of the biggest regional banks, the investment case for WF is even better. Take a look to the table “Regional and diversified banks” below.

WF ranks number 2 across a group of 26 biggest regional and diversified banks. It only comes behind SVB Financial Group which is a start-up, venture-capital focused banks. This actually makes sense since SVB’s brand is prevalent amongst the start up space which means the bank manages to obtain significant low-cost deposits from a niche market. However, regional banks would lack the scale in absolute amount of deposits that diversified banks like Wells Fargo enjoys.

Overreaction from the market

From the news of phony bank account opening by 5300 employees of Wells Fargo, the market is overreacting to an uncertain prospect where the bank may lose customers in the future. Well how much the bank would lose is one question that none of the market participants have attempted to quantify. So I went to quantify it to see if it actually was that bad.

For the overreaction in the market to be justified, ie its low-cost funding source aka deposits has to fly away, the bank would need to lose $77bn in deposits (% of funding source dropped 5% from 77%-current level to 72%) and for WF to be as uncompetitive as other diversified banks, $218bn in deposits have to disappear (% of low cost funding sources dropped from 77% to 64% – levels seen in JP Morgan, Bank of America). To lose $77 bn in deposits and $218bn in deposits respectively, there have to be a closure of 4mn and 12mn saving and checking accounts respectively. This is based on assumptions that 1 saving account has $26,000 in it (US total saving deposits/US population) and 1 checking account has $3,500 (in line with average cash balance held in American banks)

To have 4mn and 12mn accounts to be closed, with the current number of accounts being affected by the scandal at 114k accounts, this translates to 2 things:

- For me to worry, 1 affected customer would have to somehow “convince” 18 others to close their accounts (4mn/114k/2) – assuming 1 person has 1 checking and 1 saving account

- For me to sell Wells Fargo stocks, 1 affected customer would have to somehow “convince” 52 others to close their accounts (12mn/114k/2)

Subjectively, one can argue that it is difficult for one affeted customers to “convince” 18/52 others (including on average 13 relatives) to close 2 accounts with WF (despite the fact that closing saving account would be harder due to opportunity costs foregoing the interests that could be earned if the money was parked there until the end of saving term). Yet others may think that to “convince” 18 others may not be that hard at all.

For now, these 2 numbers give me great comfort to hold on to the shares of the 164-year-old American bank.

Valuation

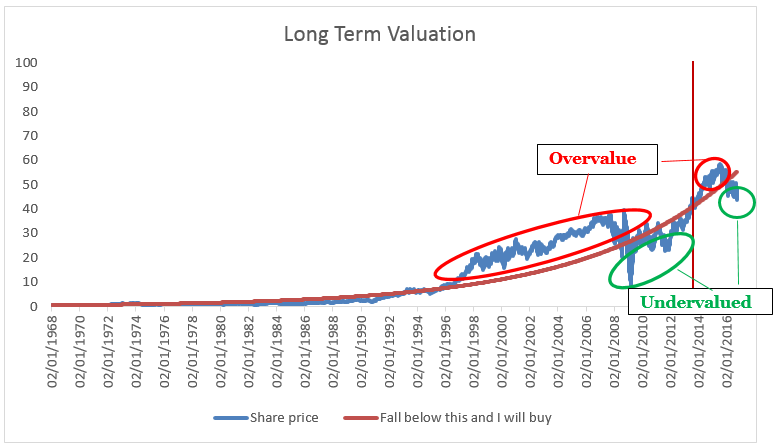

The “Long Term valuation” graph shows you how I “time” my entry point.

I will write about my valuation approach in another post, but for this article, the short version is:

WF’s price falls below the orange line which is what WF’s stock price should be in an ideal world. The orange line is obtained by multiplying WF’s price when it was first listed with the theoretical CAGR of 10%. This 10% is the worst case scenario of mine, which basically means that the stock should always grow at 10% every year. Now that the share price has fallen below this line, it means WF is undervalued. In fact, WF’s stock has never been this cheap since the end of 2013!

So those are the 4 key reasons why I bought WF. There are 2 other important factors that contribute to the buy case for WF as well and in short, these are:

- Biggest asset under administration and management amongst all banks ($2trillion) which contribute significantly to the stickiness (switching cost) of banks’ customers

- Second best in risk management measured by net charge off ratio and loan composition (which customers the banks lend to)