My paper record for the first half of 2019 looks poor.

For the global portfolio, the paper record falls behind the S&P 500 (GBP, net including dividends) by 5.8% as our top 2 largest holdings underperformed the S&P 500: Alphabet and Berkshire. My thoughts are that owning exceptional companies with awesome return on tangible capital, and not paying too high a price for these companies make lots of sense. I intend to adopt this as a lifetime policy to sensible investing. All of my holdings reported satisfactory results in q1, and I’m happy with their progress. Google continues to delight billion users with small upgrades on their digital real estate, Berkshire continues to produce prodigious amounts of cash from its diverse portfolio of businesses and stocks fuelled by world class insurance underwriting, Apple continues to focus on design and superior customer service and spent $100bn in buying back its stock, Unilever continues to woo 2.5 billion consumers everyday with 13 1-billion euro brands, and Visa continues to displace cash transactions in a $40 trillion consumer market and lots of trillions in B2B markets. As a part owner of these businesses, I continue to be amazed and inspired by the exemplar of the business leaders that lead these companies. I am fully invested in these 5 names, meaning I have significant portfolio concentration on them.

Over time I hope I will get better as an investor to be able to take large positions in smaller companies whose by default have the mathematical advantage of growing fast from a lower base. I did have such an opportunity to buy Intuit – a company that I learned from Mr Nick Train and have been an admirer of the company for 3 years. The opportunity showed up in q4 2018 when the stock traded at 22x pre tax earnings. I remember telling myself “let’s wait until it gets down to 20x, nice rounded number and I will start buying”. Looking back that was just dumb.

Now the bad bad news, for the Vietnamese portfolio, our record is significantly behind the VNINDEX. Our family equity portfolio – which stands around 5-10% of my parents’ net worth falls behind the VNINDEX by 14%. This poor paper record is the result of 1/ the recent debacle at the shareholder meeting of Coteccons (HOSE:CTD) – our largest holding and 2/ the delay in construction project approval in 2019 which impacts CTD and Binh Minh Plastics (HOSE:BMP) – a plastic-pipe producer which is also our third largest holding.

This begs the question: was our decision to invest in Coteccons wrong?

Let’s recap: Coteccons is the largest general contractor in Vietnam, having built some of the most famous residential and commercial buildings. One can simply go to the city center of Sai Gon, look up and here it is Landmark 81 – the tallest building in Vietnam.

Now general contractor’s main moat does not necessarily come through size. Our understanding of what makes a good contractor are learnt from reading the outstanding work at the Kiewit Corporation – one of the best general contractors in the United States.

Most general contractors go under because of “debt and low bidding”. The ones that have enough discipline to do otherwise eventualy do fine.

1/ Always maintain financial conservatism. Kiewit corp thrived through many cycles by holding no financial debts. General contractors earn thin margin, and if there is another party that have a “claim check” on the company’s earnings there’s one more stakeholder too many!

=> Coteccons is that rare general contractor in Vietnam, and even the world, that haven’t had any financial debt since 2010 – when it was first IPO. This is the decision of the Management, and especially of Mr. Nguyen Ba Duong – The company’s founder and current Chairman who famously said in one of his interviews, with a typical tone of a contractor: “Do not be a slave to the bank”.

2/ Bid at the right price: There’s always an urge to submit low bids to win new projects quickly. This is somewhat similar to insurance where insurers are incentivised to charge low premium to write lots of insurance policies quickly. The lovely money comes in fast but “that is the last time you are going to have any money”

=> Coteccons have maintained 4% – 7% ebit margin, and never suffer any loss as a result of low bidding. The margin is a bit lower compared to the great Kiewit Corp mainly because Coteccons started out constructing residential and office buildings while Kiewit has been constructing lots of high margin projects such as nuclear plant, hydropower plants, O&G plants, etc. This is because Vietnam is in the early stage of growth so there are still lots of opportunities left for constructing residential buildings (a Vietnamese lives in a 24m2 vs 50m2 in China or 80m2 in America)

Ok, good stuff, but what has caused the stock price to go down in the first half of the year:

Ricons proposed merger: Prior to the 2018 shareholder meeting in April 2019, Coteccons put forward a plan to acquire its associate company – Ricons via using its own stock. Retail shareholders have been expecting this merger to be approved so Coteccons can grow quickly. In addition, since Mr Duong’s wife and other CTD executives have stake in Ricons which have grown pretty quickly in the past, there were concerns if CTD Management had a “backdoor plan” at Ricons. At the 2018 shareholder meeting, Kutsocem – the largest shareholder of Coteccons rejected the merger proposal, saying that the deal wouldn’t make strategic sense and using stock is not a good idea when CTD stock price had not reflected the true value of the company. The failed expectation triggered two days of 7% drop in the stock price and continued spiral the stock down another 25%.

Delay in construction project: there have been construction project delay in the first half of 2019. This impacted most of construction material and construction companies as pending inventory/receivables built up. Many suspect that this was linked to the recent government action to clamp down on corruption. We welcome such positive governmental development but it does hurt our short term paper record.

Regarding the delay in construction project, we already expect lumpy results when we first invest in a cyclical industry such that of a general contractor. We finally got more comfort over this after seeing Coteccons becomes very flexible in winning bidding in the industrial-park space. Its revenue share from residential construction dropped from 60% in 2017 to c.30% in 2018 while its industrial revenue share roughly doubled in a matter of a year while maintaining a flat revenue growth.

Now the Ricons question: My attitude towards this is: with or without Ricons, will Coteccons survive the long-term competition? And the answer is yes due to their track record in the first 2 advantages we lay out above and a properly aligned management team: Mr. Nguyen Ba Duong wealth in the stock is worth $18m – That is an enormous sum for a country whose GDP is 2,500 USD per annum per person and the CEO – Mr Nguyen Sy Cong owns $9m worth of stock. From our assessment of the two men, we hold high regard that they do love constructing buildings and they do enjoy building the company. My parents are contractors themselves and hell did Mr Duong sound like my dad on the construction sites: straight-talking builders.

“But management is thinking of using stocks to buy Ricons when their stock price is already low, does that make sense?” Shareholders of CTD haven’t received information around what management considered as a fair price for Ricons, however, prior to the meeting, Coteccons was trading at 6x ex-cash, and if Ricons was to be valued around the typical earning multiple of contractors in the region – 8-10x, then my view is that, selling a bit of 6x stock to buy a fast growing 8-10x stock isn’t crazy, in fact it may just look quite enticing. So we are not against using stock, but if we can influence management, we would prefer them using the huge amount of cash that they have on the balance sheet.

Ok, so what was the price that we paid:

The stock is currently a 20% position in our portfolio, at an average cost of 126,000 VND a share – equivalent to 4.7x pre-tax earnings, excluding cash. At our average cost, 40% of the stock is in cash with no debt. Should we be excluding the cash? Yes because we simply can’t predict interest rate. Interest rate can go to 20% or down to 1%. We made no attempt in predicting interest rate. We would view the cash separately as a “business” whose earnings year to year we can’t predict, but whose minimum worth we can estimate with reasonable confidence.

=> We really hope that Coteccons will consider a major share buyback. It did buy back stock in early 2019, around 4% of its share counts. It has enough cash to buy back 50% of its share counts.

The stock is at 3.2x pre-tax earnings, and we are contemplating even adding further to it.

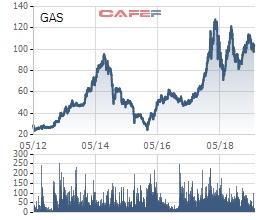

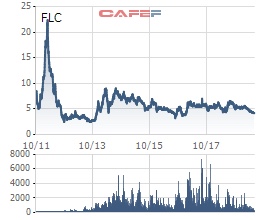

We have observed out of whack stock price behaviours in Vietnam. All sort of weird behaviours in many large blue chip companies like:

HOSE:GAS

HOSE:MSN

Or HOSE:FLC

We don’t predict stock price, but we are cognisant of the extreme volatility in Vietnamese stocks, driven largely by retail investors. Mr Buffett used to say that volatility is an advantage to the long term investors. Overtime we will see if we really can take advantage of it in the Vietnam market.

Over a long time, we think that if we get to buy good companies at a reasonable price, the stock will eventually follow the company fundamental developments. It will then rest upon our logical reasoning and facts to determine if we are right in the end, or if we are just stubborn trying to be right along the way. It is also possible that we get plagued by confirmation bias.

So we take comfort that as long as Coteccons keeps building large-scaled structures, keep biding at the right price, keep maintaining financial conservatism, then our 4.7x pre-tax earnings looks extremely enticing.

As of now, we have a paper loss of 17% in CTD, but for now we view that as Mr Market has thrown up a nice opportunity for us. Time will tell if we are right.