The followings will be covered in this post:

- My recent trip to Berkshire Hathaway Annual Meeting 2018

- Some words on the saving and investing journey so far

- Performance

- Some books and readings in review

Berkshire Hathaway Annual Meeting 2018

Around mid- July 2017, I got to meet David whom I have introduced in some of the previous posts. David’s partnership letters have been one of the most comprehensive, detailed and eye-opening letters I have read in my short career as a part-time private investor. David urged me to attend the Berkshire Hathaway meeting and so after some hesitation I decided to buy the ticket, get the visa, pack my bags and go.

Joined with me was a good friend who was studying in Washington, DC at the time. We both enjoyed the journey of value investing and so both decided to attend the Berkshire event for the first time.

After having spent the Thursday evening feeling a bit lonely, I woke up on Friday with full energy, ready to explore this town. I had got to go check out the Nebraska Furniture Mart – a very famous investment Mr. Buffett invested back in the 1980s.

Following a rather quiet morning, I and my friend both went to downtown Omaha. Omaha struck me as a very quiet town, it’s hard to think that it is where the most successful money manager and business collector lives.

I went to check out the place that houses Berkshire Hathaway’s headquarter – Kiewit Plaza, and of course I had to pay a visit to Warren’s private house. It looks like any other house in the neighbourhood…$60bn in net worth and a $300k house…this peculiarity of Mr Buffett reminds me of Charlie’s reaction to Charles Darwin – “He must have tricks that I can learn!”, and so I have got to learn a trick or two from Mr Buffett over the past 5 years.

We then went to a drink to meet with David’s mentor – Mr. James Pan. James ran his own fund some years back and now look after his own money. His track record is nothing short of magical, compounding at 17% p.a over the last 2 decades. I also met with James’s and David’s friends who all seem to be highly successful private investors. When I looked at them I had the same thought that Sam Walton had when he fondly thought of his father-in-law – “If I try hard enough maybe one day I can be like him”. It proves that “admiration love” is a powerful thing.

And then the main event. We woke up early at around 5 thinking that it would give us plenty of time to queue up and get good seats. We went to the location – Century Link Omaha and to our surprise, there were already 5 long queues. The sea of people just overwhelmed me. I saw all kinds of people, travelling from all around the world to attend this meeting. It must have been 15-20,000 people in attendance.

2018 meeting 4 key lessons:

“We like having individual shareholders and we don’t favour institutions. We’re not going to give guidance and talk especially to them on investor calls. We want shareholders who are partners, basically.” – Warren Buffett

“People want to find some formula. These people want the world to be like physics. But the world isn’t like physics, outside of physics. False precision just does nothing but get you in trouble.” – Charlie Munger

“If you’d bought gold at the time of Christ and you figured the compound rate on it, it may be a couple tenths of 1 percent. Anytime you buy a non-productive asset you are counting on somebody else later on to buy a non-productive asset because they think they can sell it to somebody for more money. It’s been tried with tulips and with various things over time. And it does come to a bad ending.” – Warren Buffett

“It’s not that damned easy to duplicate. Think of how little direct copying of the Berkshire system there’s been” – Charlie Munger

10 lessons from Berkshire Hathaway Meeting record (courtesy to CNBC for the collection of Berkshire past meeting – the best lecture on investing anyone can get)

1994 – “Derivatives lend themselves to the use of unusual amounts of leverage and they’re not completely understood by the people involved. Anytime you combine ignorance and borrowed money you can get some pretty interesting consequences” – Warren Buffett

1998 – “An occasional dull stretch for new buying is no great tragedy in an investment lifetime.” – Charlie Munger

1999 – Questioner “Mr Buffett, how can I make $30bn?”… “Start young” – Warren Buffett

2000 – “If you mix some legitimate development like the development of the Internet with something which is wretched and irrational such as Internet stocks, you are mixing something that has bad consequences with something that has very good consequences. If you mix raisins with turds they are still turds.” – Charlie Munger

2001 – “Anybody can generate float. If we gave our managers a goal of generating $5 billion of float next year, they could do it in a minute, but we would be paying the price for decades to come.” – Warren Buffett

2004 – “It’s a life-long game, and it you don’t keep learning, other people will pass you by.” – Charlie Munger

2008 – “Forget about the word “stock.” – Warren Buffett

2012 – “How do these super-smart people with all these degrees in higher mathematics end up doing these dumb things? To a man with a hammer every problem looks pretty much like a nail” – Charlie Munger

2015 – “Any company that has an economist certainly has one employee too many.” – Warren Buffett

2017 – “If I could only pick one statistic to ask you about the future before I gave the answer, I would not ask you about GDP growth. I would not ask you about who was going to be president. I would ask you what the interest rate is going to be over the next 20 years.” – Warren Buffett

Some words on the saving and investing journey

“I don’t intend to get rich. I want to get independent. I just overshot!” – Charlie Munger

I started my first step into this journey about 5 years ago when I interned for a brokerage house in Vietnam. It was during this time that I made my first investment, buying into a port operator in Hai Phong city called – Viconship (HOSE:VSC). It was cheap based on my financial model, which I was very proud of building at the time. It was rather complex, with multiple excel tabs and scenarios in it. As I flexed through various scenarios I realised that even in the worst case Viconship was still undervalued by 50% or so. The financial model gave me a sense of the analytical process behind an investment, though little did I know that the complexity was unnecessary, and I was just trying to use what I learned from university and from a short course that helped people break into investment banking. I later learned from Charlie that this is a very example of “Man with a hammer” tendency – “To a man with only a hammer every problem looks pretty much like a nail”…well, to a rookie analyst with financial modelling skills, every company looks like a bunch of numbers that can be punched into excel.

And then as I got my first full-time job offer to work for one of the Big 4 in London, the summer before I started I thought about investing. At the time I had known about the wonderful idea of compounding interests…I remember I would construct this excel sheet where I put in the amounts of saving I could save, a rate of return and I would try to work out my net worth at the end of 5, 10, 15 years and I would get excited about the idea that “if you underspend your whole life, make sensible investments you will eventually get rich”. It helps also too that it is very much a “high road in life”, it looks almost like an empty road. As I look around, my approach isn’t favoured by peers, for that it goes against human’s “superior” tendency, it is not protected by “social proof” and is far less likely to be subjected to constant challenge from “doubt avoidance” and “envy” tendencies. Well taking this high road looks already like a quasi-lollapalooza journey.

And so for the past 3 years when I started having real money, I began my investing journey. I first learned of Nick Train who is an outstanding investment manager in the UK. One of the quotes I remember the most from Nick was that “UK investors make mistake because they don’t listen to Warren Buffett”, and then later on David would tell me “you only need to learn about investing from Warren and Charlie”. As I dig into the track record of Mr Buffett, the wits and wisdom of Mr Munger, I realise that Mr Buffett and Mr Munger’s advice are undervalued even though they have revealed their tricks for almost 6 decades now.

Every month I would save. As of now the saving rate is currently averaging at 40% (taking into account bonus and some small monetary gifts from the parents). An upcoming promotion in a month time would get my saving rate up to 62% as I intend to not let any lifestyle inflation creeping into the process. On top of that, an ok rate of return has also been realised, which reflects me being still in the early stage of the learning process. If it takes another decade or two to learn to beat the market, so be it.

“Human Felicity is produced not so much by great pieces of good fortune that seldom happen, as by little advantages that occur every day” – Benjamin Franklin…well I guess that goes for human improvement as well.

The thought that in the next 3 years, as I’m approaching 26, I would have a net worth that would give me 1/ significant peace of mind, 2/ significant flexibility in choosing the investment manager I want to work for and 3/an option to relocate back to my home country and independently manage my money and my family’s money, it got me all excited. This is conditional upon 1/no lifestyle inflation and 2/achieve at least 10% annualised return. And to take things further, assuming a 60% saving rate is met, another 4 years of working (preferably with an investor I admire), a ok rate of return…then by the age of 30 I should be able to temporarily get off the corporate life and engage in full-time independent “passive wealth accumulation” and curiosity-driven reading.

As Ai Wei Wei has said: “When you taste freedom it will stay in your heart. And you will be more powerful than the whole nation.”

Performance

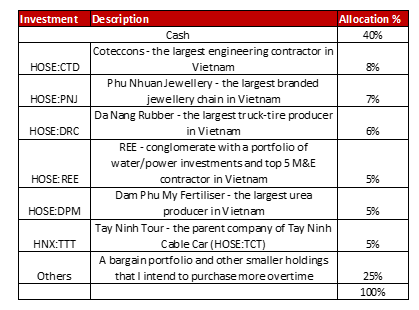

Viet Portfolio

Since inception of 06 December 2016, the Viet portfolio has achieved a 13.7% annualised return (24.6% total return), compared to 26.5% (49.8% total return) of the VNINDEX and 28.1% (53.2% total return) of the VN All Share Total return index (VNALL TRI).

YTD, the Viet Portfolio has had a +1.32% total return vs -0.9% and -0.8% of VNINDEX and VNALL TRI respectively.

Around mid-2018, my parents decided to put more money into the portfolio, an amount equivalent to 2x the original amount I initially helped them look after. More money…more responsibilities. I thank them for entrusting this portion of their net worth to me, and that they always encourage me by saying that “this is for your learning”. They set out with a low monetary expectation but with extremely high hope, so I shall do my best.

The above performance would highlight two things I have come to learn

- It’s hard to beat the market

- It’s hard to beat the market trying to diversify.

I will talk briefly about the 3 largest investments above. In the light of Mr Sandy Gottesman’s favourite approach to investment questioning – “What do you own and Why do you own it?”

Coteccons – CTD is the largest contractor in Vietnam. One could think of it as the best version the Vietnamese can give in response to Kiewit Company of America. CTD is the achievement of Mr. Nguyen Ba Duong who is the company’s CEO. As at today, he held 5% share of the company and is the chief revenue generator of the company, bringing 28,000bn VND a year worth of contracting business to the firm. As at the time of investment, CTD was trading at a 4.6x earnings net of net cash, after worry about recent margin contraction surfaced – an issue that is typical for any contractor.

PNJ – Phu Nhuan Jewellery is the largest branded jewellery chain in Vietnam. The company is an achievement of Mrs. Dung and her family. Under her tenure the company morphed into the largest branded jewellery stores after having started out as a chain of gold-bar trading shops. We started our investment back in mid-2016, the stock went up to an overvalued territory where we sold 30% of our original position. And then when the VNINDEX contracted around early 2018, the stock was on sale again. At a 16x earnings with a double-digit growth prospect in the next 3-5 years, I then topped up the position.

DRC – Da Nang Rubber Company is the largest truck tire producer in Vietnam. The company is and will be the main beneficiary of Vietnam industrialisation. As Vietnam transitions itself from an agricultural based to a more industrialised nation, there will be significant demand for transportation stemming from the growth of industrial parks and the demand of the Vietnamese consumers and businesses. In fact, road ton-kilometre of goods per capita in Vietnam is around 600, vs 4000 in China and 6000 in the US. As at the time of purchase, DRC was trading at a normalised 13x earnings. With the huge tailwind, a market leading position I think I was getting the comp for a good price.

During the quarter I was also involved in a situation which I thought to be a nice “workout” situation, but turned out my line of reasoning was inaccurate.

DHG – Duoc Hau Giang Company is the leading Vietnamese pharmaceutical company. Around late July 2018, Taisho Company – a leading Japanese pharmaceutical company offered to increase its 24.9% stake to 32%, and offered to buy DHG stock at a price that is 20% premium to the market price.

I had learned beforehand that by the Vietnamese law, when company wanted to purchase a stake of 5% or more which subsequently result in them owning larger than 25%, they would have to make a mandatory offer. As Taisho was making this mandatory offer, at a 20% premium to the market price, I thought to myself that I could buy the stock at the current price and sell them back to Taisho with a 20% profit…everything can be done in a month! And so I did.

Later I found out that the block of DHG shares that I own may not be purchased in full by Taisho. This can happen if oversubscription occurs. Example: Taisho offers to buy 9.2mn shares. If there are 15mn shares tendered, then say X is the amount I wanted to sell back to Taisho, the actual amount that Taisho is going to purchase at the mandatory offer price from me would then be: X x 9.2mn/15mn.

As I found out, 36% of my DHG block got bought by Taisho, hence there were 26mn shares being tendered…Luckily I managed to sell the remaining 64% at a price that results in the whole quasi-workout purchase producing a +2% return.

Through this one, I learned that 1/ “It doesn’t matter whether people agree with you. What matters is that your fact and logic is right” … I missed out the important fact of proportional buying from Taisho and my logic missed the fact that this is just a stake-increasing purchase, not an entire acquisition, which would have been a true workout situation. And 2/ don’t get excited. I got plagued by what Charlie called “Consistency tendency” and “Confirmation tendency”. I made the purchase hence I would want my reasoning to be consistent with my act, and some of my friends agreed with me so it has got to be right.

Lessons: 1/ I should have taken more time to think, 2/ don’t get excited…that goes for all situations and 3/ “The exploitation of special situations is a technical branch of investment which requires a somewhat unusual mentality and equipment. Probably only a small percentage of our enterprising investors are likely to engage in it.” – Ben Gram.

Global Portfolio

Top Holdings:

- Lindsell Train UK Fund

- Lindsell Train Global Equity fund

- Berkshire Hathaway

- Alphabet

- Visa

- Unilever

- Fanuc

The portfolio since inception in November 2015 has compounded at 12.5% annualised return, comparing to 20.5% of S&P GBP Total return net index (per capitaliq) and 13.9% of MSCI World USD Total return net index (per capital iq, the GBP equivalent has only been available since 2017).

This performance highlights 2 things:

- It’s hard to beat the market

- It’s easier trying to beat the market by holding a concentrated portfolio than a diversified one

A new company featuring in the top holdings is Fanuc standing for Factory Automation Numerical Control

Fanuc is a Japanese company engaging in manufacturing:

- Computer Numerical Controller (CNC)

- Industrial Robot Arm

- Robot machine tools

To ease readers ‘understanding into the above 3 products, a brief intro into the automation world is needed.

In the 1950s, CNC was invented to allow ease of programming machine tools. At the time lots of machine tools were hydraulic. Over time electrical machine tools displaced the hydraulic ones for obvious reasons (ease of use, ease of programming, standardisation, etc).

To control these CNC electrical machine tools, one would need a controller that allows for programming. Fanuc and a handful of companies tried to develop CNC controllers. The US controller manufacturers opted for the customisation path whereby their version of CNC controllers and machine tools were highly complex and very specifically adapted to customers’ specification. It is great in terms of building a switching-cost type of moat and that other manufacturers would find it hard to win customers over.

Though Fanuc opted for a much better path, and that is to develop standardised CNC controllers that could be used for any CNC machine tool. They may have lost customer specification contracts, but they came out winning the entire mass market over the upcoming 3-4 decades. As statistics showed, Fanuc slowly achieved a 70% market share in the 80s, and as of now that number remains relatively unchanged.

While CNC machine tools were taking over the factory floor, another type of “machine” slowly emerged, and that is robot. The differences between robot and CNC machine tools can be seen in the following videos:

- Robots: Fanuc Industrial Robot Arm

- CNC machine tools: FANUC drilling machine tool – Robotdrill

Well it would come to my surprise that Fanuc won in both CNC (both controllers and machine tools) and robot. Fanuc currently has 25% of the industrial robot arm market share, following behind Fanuc is ABB, Yaskawa and Kuka…aka the Big 4 of factory automation. Things got even better when we look at the CNC machine tool that Fanuc dubs as Robotmachine. Fanuc Robodrill, for example commands 80% market share of CNC drilling machines that are used to manufacture our beloved smartphones.

Over time it would be an interesting bet to see who is going to win the race of factory automation. So far, Fanuc struck me as the one in the Big 4 competition that has complete focus on controllers, industrial robots and machine tools. Fanuc avoids dwelling into other parts of automation such as software (Rockwell being the key competitor) or other electrical related sub industries such as producing electrical components (ABB for instance)…

…“Walking the narrow path” as Dr Seiuemon Inaba called it.

Who is Dr Inaba?

“In the 1980s, I visited Europe and Asia once a year to review current operations as CEO. We were in the process of trying to launch a factory automation effort, by selling the concept of factory of the future. I had admired Fanuc of Japan and its head, Dr. Seiuemon Inaba. They were the clear market leaders in numerical controls for machine tools. I asked my Japanese staff to set the stage for my meeting with Dr. Inaba in New York in November 1985. We hit it off immediately. We agreed to establish a 50/50 joint venture in factory automation. At $200 million in 1986, it was the biggest international deal that we had done in the 1980s.” – Jack Welch – the best operating manager of the late 20th century as he recalled his own defeat in the numerical controller business to Dr Inaba of Fanuc.

Dr Inaba’s mottos were and are always:

- Reliability

- Low cost

- Service

These mottos have hardly changed over the last 3-4 decades. It can be subsequently seen how these 3 mottos have produced a lollapalooza result:

- Reliability: Fanuc America president cited that a downtime of a robot would cost a company approximately $20,000 per minute. Fanuc as cited by many factory users, as the champion of reliability among robot manufacturers. “Zero downtime” is now currently underway at Fanuc’s R&D department. AI would be the main facilitator of this process.

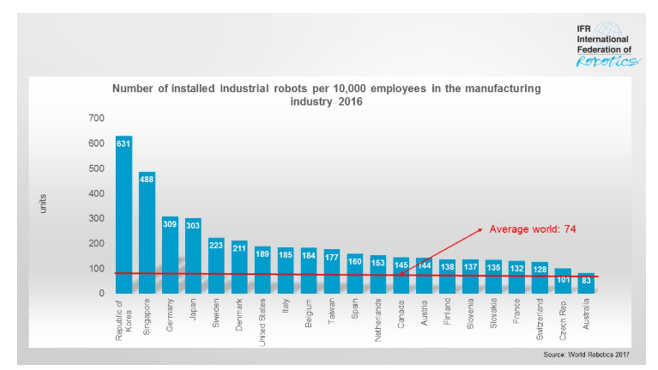

- Low cost: Fanuc’s controllers/robots are cited by many as below the market price. Well who doesn’t want cheap and reliable robots? The thing isn’t a luxury good, it is a necessity if you want to remain competitive. It is a coincidence that the UK is lacking behind Germany in terms of productivity as the robot density in Germany is 4x as much as that in the UK.

- Service: a win-win situation can be seen here. Fanuc stocks in their inventory excess amounts of parts that they can just replace faulty parts for customers rather than trying to fix it. Although it costs Fanuc in terms of inventory holding costs, the result is first-class customer service.

And the lollapalooza result: 40% operating margin and 20%+ ROE (adjusted for net cash and long-term investments).

At the time of purchase, Fanuc was trading at 20x normalised earnings (net of cash). This is a fair price to pay for the most competitive company in the automation industry, which benefits from a very visible tailwind for decades ahead. The tailwind can be summarised in the following graph:

Some readings and books

Kiewit – An uncommon company – Jeffrey L Rodengen

“getting work at the right price” + “building work at the lowest cost” + “taking care of our assets” = knockout formula for a winning contractor

Psychology of human misjudgement – Charlie Munger

Link: Mungerism v1

PDF: Mungerism v2

Berkshire Hathaway Annual Meeting Record

Link: The duel

Trupanion annual letter

Link: Very good letters!

MTB Bank annual letter

Link: What it means to be a good banker

In the plex – Steven Levy

“Just as Google had taken advantage of the oversupply of data centres in the wake of the dot-com bust it had a great opportunity to buy fibre-optic cable cheap. Google began buying strategically located stretches of fibres. We were paying ten cents of the dollar. How much fibre did Google own? More than anyone else on the planet!”

Titan – Ron Chernow

Shoe Dog – Phil Knight

Benjamin Franklin – Autobiography

“Make wisdom acquisition your moral duty” – Charlie Munger

Hey Author, enjoyed reading your post. Do you have a view on why the consumption in vietnam seems relatively weak to previous years? Vinamilk’s revenue growth has been tepid.

LikeLike

Hi Jo, thank you for visiting my blog. Appreciate it. I don’t have a good answer to why the consumption has slows down from a macro perspective. However the industry, as with any industry, is driven by who the main suppliers are. And in the Vietnamese milk industry, Vinamilk controls a big bloc of it. Hence if the consumption of milk is slowing down, there will be a huge reason attributable to Vinamilk itself slowing down.

Though I will highlight this. It is accepted fact that Vietnamese milk consumption per capita is low generally compared to others. And unless you think milk is bad for health, then you would expect eventual convergence of Vietnamese milk per capita to the world average, which is roughly 2.5-3x that consumed in Vietnam.

Secondly, Vinamilk is a hugely branded product. And so aside from volume growth there will be pricing growth that looks sure to outperform inflation rate.

Thirdly the nature of compounding interests prevent anyone to gallop ahead when they are already big. So it is obvious that if Vinamilk only constrains itself to the Vietnamese market, they will not register the kind of growth they have in the past.

My own expectation is that Vinamilk will have roughly 1% cagr going from general per capita consumption growth rate, another very small percentage (below 1%) coming from stealing couple bps of market share ( they are already very big) and potentially 3-4% pricing growth if Vietnamese inflation is to go down to 2-3% long term inflation rate from the current 4% (4% inflation rate is unsustainable, so I would expect inflation to subside to a more meaningful number, otherwise our currency would be cut in half over 2 decades, which would be very bad). So all in all I expect Vinamilk to compound their earnings at 5% rate going into a long future ahead. That would be a 20x earnings fair value estimate if I use a discount rate of 10% (which is twice as much as the Vietnamese government bond yield at the moment).

I hope this is helpful. Thanks again for visiting the blog!

LikeLike