Happy Lunar New Year!

The 2018 first blog post was delayed due to the unexpectedly busy January and first half of February over in the Vietnamese equities space.

Following 2017 massive gain of the VNINDEX, your author grew increasingly paranoid by the high valuation exhibited by top-class Viet companies.

He then devoted the entire January and first half of February to the Vietnamese portfolio.

Before going into the details, I just wanted to remind readers that the Vietnamese portfolio comprises of 5% of my parents’ net-worth and 10%-15% of my brother’s net-worth.

If anything, I do the utmost I can to not lose them any money, with an intention that over time I will compound this at a sustainably good rate.

I expect during such period, while return is a goal, the objective of this management, as agreed with the parents and the brother, is that I will learn everything that I could about companies and stocks. If Mr. Warren Buffett is still learning at his late 80s, it will be just stupid for me – a “millennial” to not place “learning” as my top priority.

During such learning period, reader can expect that the Break’investor will make several acquaintances with great investors.

As David (Mr.L), whom I normally describe to my friends as my “investing mentor”, advised me to “keep writing to great investors”. So I did… (for those who do not know who David – Mr. L is, please visit this blog post here and here)

…And that leads me to the first topic of this post

Mr. M

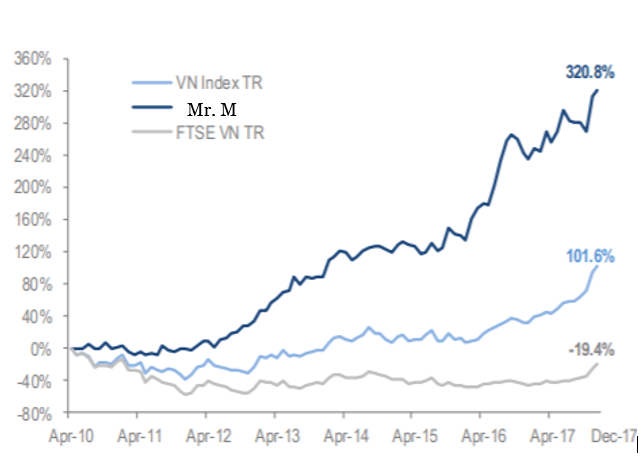

Mr. M is an exceptional fund manager. In spite of being a foreigner to Vietnam – a country that is vastly different to Mr. M’s hometown (think European countries), he spent more than a decade in Vietnam learning and investing in Vietnamese companies. He and his fund’s track record is nothing short of magical:

*don’t look at it too closely, it made my little over 1 year track record looks very bad…*

Now I’ve got to know Mr. M by stalking his fund’s portfolio around mid-2017.

I cannot be thankful enough for knowing Mr. M. Out of the 3 Vietnam-based fund managers I wrote to, Mr. M was the only one who was generous enough to reply to my email…and it wasn’t just a casual “Hey thank you” note, it was a genuine one that shows his interest in knowing me better as an investor.

The months following his reply, I exchanged dozen of emails with him, talking either about general investing concepts or just outright pitching stocks.

I expect to learn a lot from him.

The first lesson he (subtly) taught me was his fund’s focus on fundamentally sound stocks, with a hint towards industrialisation as a tailwind theme.

Had I not taken David’s advice – “investing is a humbling game”, I would have missed out this tailwind. Because I would have not sought after Mr. M’s knowledge. I would have just stood by, watching him in the dark without proactively learning from him.

I cannot be thankful enough for David’s wise consultation; thanks to him, I’ve got to know Mr. M!

Knowing Mr. M led me to another big idea for 2018, which is our family’s stock purchase of DRC – the largest truck-tire manufacturer in Vietnam. Mr. M, as part of his fund newsletter to investors, included me in this distribution and one day, sent me his note on DRC. This company, thanks to industrialisation, is enjoying a seemingly massive tailwind, both short and long-term ahead of it. In the short to medium run, DRC takes advantage of the transition between bias tires to radial tires, thereby raising truck-tire standard, in effect directly attacking the poor-quality imported tires and challenging the high-priced tires made by the giants (Bridgestone and Michelin). Then in the long run, if we look at the amount of freight transported by road, measured in ton-kilometre per capita, then Vietnam stands at about 600, meaning for 1 person in Vietnam resulting in a 600 ton-kilometer road-based freight demand, vs 4000 in China, 9000 in the US and some 2000-4000 in Europe. If ton-kilometre of road-based freight transportation can ever be a proxy to truck-tire growth (which I think it sensibly is), then DRC will be a big beneficiary.

Such purchase of DRC reflects my 2 lessons, 1 I learned from Mr. M (pay attention to industrialisation in Vietnam) and 2 I learned from David and Mr. Warren Buffett (position myself in tailwinded industry).

I then quickly made my mind to make DRC one of the biggest positions of the Vietnamese portfolio.

Bargain portfolio

David’s wise consultation suggests me to explore ideas/investment philosophies using my facts and logics.

Facts and logics point me away from purchasing high-valuation companies (25x PE~) even if they are of outstanding quality (Vinamilk)…

…and facts and logics told me to NOT rely on mainstream valuation multiple (Headline PEx on the web) and any other headline valuation metrics for that matter.

A standardised PE is a very dangerous tool to use. Companies exist in different shape and size, led by either nutcase CEO or exceptional CEO, commanding great advantage or poor economic characteristics, financially healthy or malnourished, given all these seemingly differences in every company, a standardised metric will never do any company’s value justice.

I learned to look beyond that…

…and the result was that I found a bunch of bargain companies (and even quality company) trading at 0-3x “hidden” PE, that if bundled together, as advised by a notable “eminent dead” (to paraphrase Mr. Charlie Munger) – Mr. Ben Graham, will eventually “work out”, as practiced by Mr. Warren Buffett…

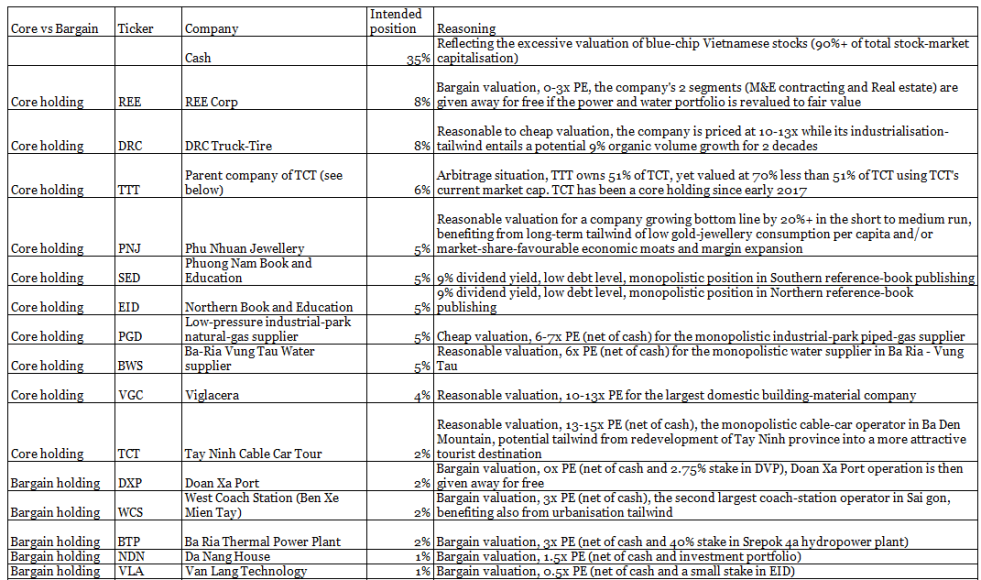

…and so I’m currently having quite a few of them. Find below for the current portfolio with “core holding” meaning long-term investments and “bargain holding” meaning the bundle of stocks I expect them to work out as a group.

However, readers will notice a stark difference to the portfolio, which I reported just about a month and a half ago (see this blog post here). This is because of the significant change in valuation and attractiveness of Vietnamese companies following a year where the VNINDEX registered a 50% gain – an unheard-of gain in Vietnam and very rare gain even in global equities space. If you come across 10 stock markets globally that registered 50%+ gain in any single year in their past, please notify me.

I therefore remain moderately defensive with respect to Vietnamese stocks in 2018.

So that is that. I’m now back to the global portfolio (my own portfolio) and continue my search for exceptional company with capable management and reasonable valuation.